Pay Off Mortgage Faster Calculator – Save Thousands, 100% Free to Use, No Signup Needed

Use our 100% free pay off mortgage faster calculator to save thousands in interest, shorten your loan term, and compare repayment strategies instantly.

Payoff Mortgage Faster Calculator

Provided by Lifegic.com

Own Your Home Sooner: Discover the Power of Our Pay Off Mortgage Faster Calculator

Ever wondered how much faster you could own your home free and clear? This powerful pay off mortgage faster calculator shows you in seconds how simple adjustments to your repayment strategy can dramatically cut years off your loan and save you thousands in interest. If you’re looking to escape the burden of mortgage debt and achieve financial freedom sooner, our pay off mortgage faster calculator is your essential tool.

What Is a Pay Off Mortgage Faster Calculator?

A pay off mortgage faster calculator is an online tool designed to help homeowners visualize and plan accelerated mortgage repayment strategies. Instead of simply relying on your bank’s standard amortization schedule, this calculator empowers you to explore how various actions—like making extra payments, switching to a biweekly schedule, or applying a lump sum can impact your loan term and the total interest paid over the life of your mortgage.

It’s for anyone with a mortgage: from recent homebuyers eager to build equity quickly, to seasoned homeowners looking to reduce their financial obligations before retirement, or even those considering a refinance. It matters because understanding these impacts can translate into significant savings and a faster path to debt-free homeownership

Step-by-Step: How the Pay Off Mortgage Faster Calculator Works

Our pay off mortgage faster calculator simplifies complex financial calculations into an easy-to-understand process. Here’s a breakdown of the key inputs and how your contributions influence the outcome:

Extra Monthly Payments

This is one of the simplest yet most effective ways to accelerate your payoff. By adding a consistent amount to your regular monthly payment, you directly reduce your principal balance. Since interest is calculated on the remaining principal, a smaller balance means less interest accrues over time.

- Example: Imagine your standard monthly mortgage payment is $1,500. If you consistently add an extra $100 each month, your actual payment becomes $1,600. That extra $100 goes straight to reducing your principal, leading to a faster payoff and substantial interest savings.

Biweekly Payment Strategies

Instead of making one large payment each month, a biweekly strategy involves making half of your monthly payment every two weeks. Since there are 52 weeks in a year, this results in 26 biweekly payments, which effectively means you make 13 “monthly” payments per year instead of 12.

- Example: If your monthly payment is $1,500, you’d pay $750 every two weeks. Over a year, this amounts to $750 x 26 = $19,500, compared to $1,500 x 12 = $18,000 with monthly payments. That extra $1,500 annually (one extra monthly payment) is channeled directly to your principal, significantly reducing your loan term and total interest.

Lump Sum Payments with Date Selection

A lump sum payment is a one-time, additional payment made towards your mortgage principal. This could come from a work bonus, an inheritance, a tax refund, or any unexpected windfall. The calculator allows you to specify both the amount and the exact date you plan to make this payment.

- How it works: When you input a lump sum payment and a specific date, the calculator applies this amount to your outstanding principal on the next payment date after the specified date. This immediate reduction in principal means that all subsequent interest calculations will be based on a lower balance, leading to quicker amortization and interest savings.

- Example: You receive a $5,000 bonus in June and plan to apply it to your mortgage. If your next payment date is July 1st, the calculator assumes the $5,000 will be applied then, immediately dropping your principal and recalculating the future interest.

Refinance Scenarios

Refinancing involves taking out a new loan to pay off your existing mortgage, often to secure a lower interest rate or change your loan term. Our pay off mortgage faster calculator lets you model these scenarios by entering a new interest rate, a new loan term, and any associated closing costs.

- Example: You have a 30-year mortgage at 4.5% interest. You can use the calculator to see what happens if you refinance to a 15-year mortgage at 3.0% interest, factoring in $3,000 in closing costs. The calculator will show you the new monthly payment, the revised payoff date, and the total interest paid under the new terms.

Lifestyle Savings Options

This unique feature allows you to identify potential monthly savings from your lifestyle (e.g., cutting down on dining out, subscriptions, or daily coffees) and automatically apply those savings as extra payments towards your mortgage. This helps integrate debt acceleration into your daily budgeting.

- Example: You identify that you could save $50 a month by packing your lunch instead of buying it. By checking the “Apply lifestyle savings” box, this $50 is automatically added to your extra monthly payment, without you having to manually input it each time.

Currency Support (Multi-Country)

Our calculator is designed for global use. You can select your preferred currency (USD, EUR, GBP, INR, CAD, AUD) to ensure that all financial figures, from loan amounts to interest savings, are displayed in a format familiar and relevant to you.

Full Amortization Schedule and Interest Savings Breakdown

After inputting your details, the calculator generates a comprehensive amortization schedule. This table breaks down each payment into principal and interest components, showing your remaining balance over time. It also provides a clear breakdown of how much interest you save and how much earlier you pay off your loan compared to your baseline scenario.

- Understanding the Breakdown: You’ll see your original projected payoff date versus your new accelerated payoff date. The “Total Interest Paid” will highlight the difference, clearly illustrating the financial benefits of your chosen strategy. This transparent view helps you make informed decisions about your mortgage.

Calculator Core Features

Our pay off mortgage faster calculator isn’t just about crunching numbers; it’s about providing clear, actionable insights through a suite of intuitive features:

- Sticky Summary Bar: Keep an eye on your key results, like new payoff date and total interest saved, no matter where you scroll on the results page.

- Share/Export to PDF: Easily save, print, or share your personalized payoff report with financial advisors or family members.

- Smart Repayment Tracker: Visually track your progress with a dynamic bar that shows how much principal you’ve already paid off.

- Dynamic Strategy Comparison: Quickly compare different payoff methods (e.g., biweekly vs. extra payments vs. lump sums) side-by-side to find the best fit for your financial goals.

- Timeline: See key mortgage milestones, including your start date, lump sum payments, halfway point, and payoff dates, presented chronologically.

- Charts: Visualize your loan balance reduction and total interest paid over time with easy-to-understand graphs.

- Instant Result Updates and Reset Button: Get immediate feedback as you adjust inputs and easily revert to default settings with a single click.

Use the Pay Off Mortgage Faster Calculator to test biweekly payments, lump sums, refinancing, and more. Uncover thousands in interest savings and shave years off your mortgage.

A Note on Accuracy for Our Pay Off Mortgage Faster Calculator

Our pay off mortgage faster calculator uses industry-standard formulas to provide highly accurate estimates based on the information you provide. While we strive for precision, it’s important to remember that these calculations are for informational and planning purposes. Real-world scenarios can vary due to factors like:

- Rounding Differences: Minor differences may occur due to how various financial institutions round interest calculations.

- Payment Processing Times: The exact date your payments are processed by your lender can slightly affect interest accrual.

- Escrow Account Changes: Fluctuations in property taxes and home insurance premiums (often part of your monthly mortgage payment if you have an escrow account) are not factored into the core loan amortization.

- Prepayment Penalties: Some older or non-standard mortgages might have penalties for making extra payments. Always check your loan agreement.

For the most precise figures related to your specific loan, always consult your mortgage lender or a qualified financial advisor.

Examples & Visuals

To illustrate the power of our pay off mortgage faster calculator, let’s walk through a couple of common scenarios.

Example 1: The Power of a Small Extra Payment

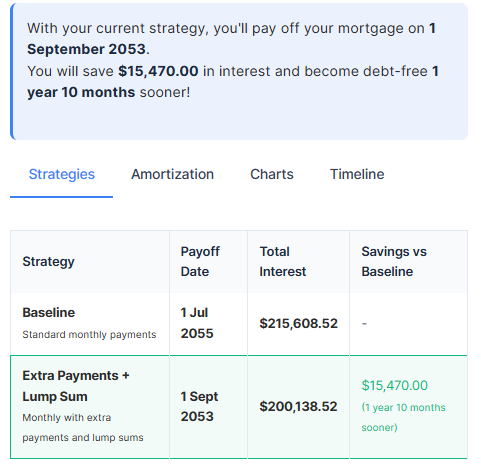

Imagine a homeowner with a 30-year mortgage for $300,000 at a 4.0% interest rate.

Baseline Scenario:

- Loan Amount: $300,000

- Interest Rate: 4.0%

- Loan Term: 30 years

- Standard Monthly Payment (EMI): $1,432.25

- Total Interest Paid: $215,610.74

- Payoff Date: July 1, 2055

Now, let’s see what happens if this homeowner adds just $50 to their monthly payment.

Accelerated Scenario (Extra Monthly Payment of $50):

- Extra Monthly Payment: $50 (total payment $1,482.25)

- New Total Interest Paid: $200,138.52

- Interest Savings: $15,470

- New Payoff Date: September 1, 2053

- Time Saved: 1 years and 10 months

The image above clearly shows how even a modest extra contribution can significantly reduce your interest burden and get you mortgage-free sooner.

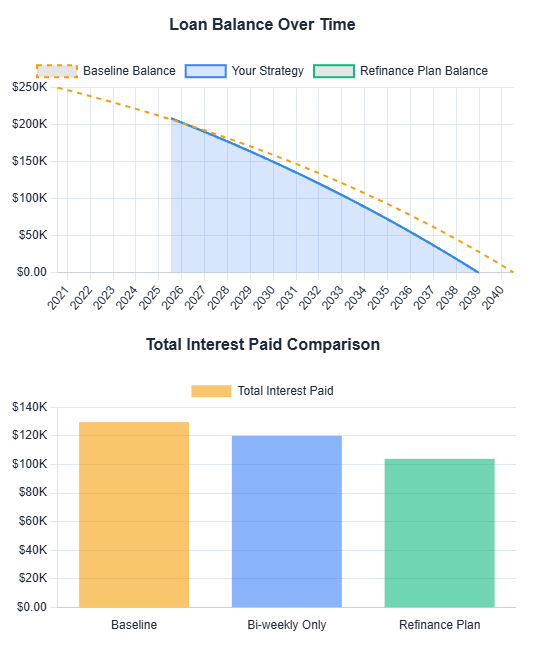

Example 2: Refinance vs. Biweekly Payments

Consider a homeowner with a 20-year mortgage for $250,000 at a 4.5% interest rate, 5 years into their loan.

Baseline Scenario (Current Loan Status):

- Original Loan: $250,000 @ 4.5% for 20 years

- Current Balance (after 5 years): Approximately $206,000

- Remaining Term: 15 years

- Standard Monthly Payment: $1,582.00

- Remaining Interest (from current point): Approximately $77,000

- Original Payoff Date: July 1, 2040

Scenario A: Biweekly Payments

- Apply Biweekly Payment strategy to the current loan.

- New Total Interest (from current point): Approximately $68,000

- Interest Savings: approx $9,500

- New Payoff Date: November 2, 2038

- Time Saved: 1 year and 7 months

Scenario B: Refinance

- Refinance Loan Amount: $206,000 (current balance)

- New Interest Rate: 3.5%

- New Loan Term: 15 years

- Closing Costs: $2,500 (added to loan principal)

- New Monthly Payment: Approximately $1,490

- New Total Interest (from refinance point): Approximately $59,000

- Interest Savings (vs. original remaining interest): Approximately $19,000

- New Payoff Date: July 1, 2040

Figure: Loan Balance Over Time and Interest Comparison

This chart illustrates how different strategies—standard monthly payments (baseline), biweekly payments, and a refinance plan—impact your loan payoff and total interest costs.

The line chart shows how quickly the mortgage balance decreases over time for each approach.

The bar chart compares the total interest paid under each strategy.

As shown, refinancing leads to the lowest total interest and fastest balance reduction, while biweekly payments also yield substantial savings without refinancing.

Use our Pay Off Mortgage Faster Calculator to explore what works best for your situation.

Benefits of Paying Off Your Mortgage Early

Using a pay off mortgage faster calculator to accelerate your loan repayment offers a cascade of benefits that extend beyond just saving money.

Financial Benefits

- Massive Interest Savings: This is the most direct and often largest benefit. By reducing your principal balance faster, you pay interest on a smaller amount for a shorter period, saving potentially tens or even hundreds of thousands of dollars.

- Increased Equity: As you pay down your principal faster, your ownership stake (equity) in your home grows more rapidly. This means you have more accessible wealth in your home, which can be leveraged if needed (e.g., for home renovations or as a safety net).

- Improved Cash Flow (Post-Payoff): Once your mortgage is paid off, a significant portion of your monthly budget is freed up. This newfound cash flow can be directed towards other financial goals, such as retirement savings, investments, or discretionary spending.

- Debt Reduction: Paying off your mortgage eliminates your largest debt, improving your overall debt-to-income ratio and potentially your credit score.

- Lower Financial Risk: Without a mortgage payment, you’re better insulated from unexpected financial hardships like job loss or medical emergencies. Your primary housing cost (property taxes and insurance) becomes significantly smaller.

Emotional and Lifestyle Benefits

- Peace of Mind: There’s immense psychological relief in knowing your home is truly yours. The absence of a large monthly payment can reduce stress and anxiety.

- Freedom and Flexibility: A mortgage-free life offers greater flexibility. You might feel more comfortable taking career risks, moving to a new city, or even retiring early, knowing your housing is secure.

- Legacy for Your Family: Leaving a mortgage-free home to your heirs can be a powerful financial gift, providing them with a secure asset.

- Simplified Financial Life: With one less major bill, your financial management becomes simpler and less demanding.

Strategic Benefits

- Accelerated Wealth Building: The money saved on interest and freed up from mortgage payments can be reinvested, further accelerating your wealth accumulation.

- Opportunity Cost: While some argue that investing the money might yield higher returns, paying off a mortgage early is a guaranteed return (equal to your interest rate) with no risk, which can be a valuable part of a balanced financial strategy.

If you have a mortgage and a desire to own your home sooner, this mortgage calculator with extra payment is for you.

Common Mistakes to Avoid

While paying off your mortgage early is generally a smart move, there are pitfalls to avoid. Our pay off mortgage faster calculator helps you compare scenarios, but here are some common mistakes to be aware of:

- Ignoring Emergency Savings: Don’t throw every extra dollar at your mortgage if it means depleting your emergency fund. Always maintain 3-6 months of living expenses in an easily accessible savings account. Life happens, and you’ll want a buffer.

- Overlooking High-Interest Debt: Prioritize paying off high-interest debts like credit card balances or personal loans before accelerating your mortgage. The interest rates on these debts are typically much higher than mortgage rates, so tackling them first will save you more money.

- Refinancing Too Often or for the Wrong Reasons: While refinancing can save you money, doing it too frequently can erode your savings with repeated closing costs. Refinance only when the savings significantly outweigh the costs, and be wary of “cash-out” refinances that increase your principal unless for a strategic, high-ROI purpose.

- Not Comparing Scenarios: Don’t just pick one strategy (e.g., biweekly) without comparing it to others (e.g., extra payments, lump sums). Use the pay off mortgage faster calculator to model various combinations and find the optimal path for your finances.

- Forgetting About Property Taxes and Insurance: Even after paying off your mortgage, you’ll still be responsible for property taxes and home insurance. Factor these ongoing costs into your post-payoff budget.

- Neglecting Retirement Savings: For some, contributing more to retirement accounts (especially if your employer offers a match) might be a better use of funds than aggressively paying down a low-interest mortgage. Balance your goals.

- Not Communicating with Your Lender: When making extra payments, clearly specify that the additional funds should be applied to the principal. Otherwise, your lender might simply hold the money or apply it to your next regular payment.

Underestimating Opportunity Cost: For some, investing extra money in the stock market might yield a higher return than the interest rate on their mortgage, especially if their mortgage rate is very low. This is a personal decision based on risk tolerance and financial goals.

Who Should Use pay off mortgage faster calculator?

The pay off mortgage faster calculator is a versatile tool beneficial for a wide array of homeowners:

- First-Time Buyers: Gain immediate insight into how even small extra payments from day one can drastically shorten your loan term and save you a fortune over decades. It’s never too early to start smart habits.

- Homeowners Nearing Retirement: Strategize how to eliminate your largest monthly expense before you stop working. This calculator can help you pinpoint the exact lump sums or extra payments needed to become mortgage-free by your retirement date, providing immense peace of mind in your golden years.

- Families Managing Two Incomes: Coordinate how both incomes can contribute to accelerated mortgage payoff, optimizing the impact of combined financial power through consistent extra payments or planned lump sums.

- Financial Independence / Early Retirement (FIRE) Planners: A mortgage is often the biggest hurdle to achieving financial independence. This calculator is a cornerstone tool for FIRE enthusiasts, helping them model scenarios to shed mortgage debt as quickly as possible and reach their freedom date sooner.

- Anyone Considering Refinancing: Objectively compare the total cost and payoff impact of a refinance against your current loan and other acceleration strategies.

- Individuals with Variable Income: Plan how to apply bonuses, commissions, or other irregular income streams as lump sum payments for maximum impact.

- Budget-Conscious Homeowners: Identify how small lifestyle savings can be rerouted to your mortgage, turning everyday habits into significant financial gains.

Step-by-Step Guide: How to Use Pay Off Mortgage Faster Calculator

Using our pay off mortgage faster calculator is straightforward. Here’s a guided tour of each section to help you maximize its potential:

- Loan Details

This is where you tell the calculator about your existing mortgage.

- Currency: Select your local currency from the dropdown menu (e.g., USD, EUR, GBP). All results will be displayed in your chosen currency.

- Loan Amount: Enter your current outstanding mortgage balance. If you’re just starting, this will be your original loan amount.

- Interest Rate (%): Input the annual interest rate of your mortgage.

- Loan Term (years): Enter the original total term of your mortgage (e.g., 15, 20, 30 years).

- Start Date: Select the date your mortgage began. This is crucial for accurate amortization calculations.

- Monthly Housing Costs (Optional)

This section helps you understand your total housing burden, beyond just principal and interest. While these costs don’t directly accelerate your mortgage payoff, they are vital for comprehensive financial planning. This section is collapsed by default; click the header to expand it.

- Property Tax (Annual): Your yearly property tax amount.

- Home Insurance (Annual): Your yearly home insurance premium.

- HOA Fees (Monthly): Any Homeowners Association fees you pay each month.

- PMI Insurance (Monthly): Private Mortgage Insurance, if applicable.

- Other Fees (Monthly): Any other regular monthly housing-related costs.

The mortgage calculator will factor these into an “Estimated Monthly Housing Cost” shown in the results, providing a fuller picture of your expenses.

- Payoff Strategy

Here’s where you experiment with different ways to accelerate your payoff.

- Pay Biweekly: Check this box if you want to implement a biweekly payment schedule.

- Extra Monthly Payment: Enter any consistent additional amount you plan to pay each month.

- Potential Monthly Lifestyle Savings: Input an amount you believe you can save monthly from discretionary spending.

- Apply lifestyle savings to extra payments: Check this box to automatically add your lifestyle savings amount to your “Extra Monthly Payment.”

- Lump Sum Payments (Optional)

This section allows you to plan for one-time extra payments. This section is collapsed by default; click the header to expand it.

- Add Lump Sum Payment button: Click this to add rows for individual lump sum payments.

- Amount: Enter the amount of each lump sum.

- Payment Date: Select the date you expect to make each lump sum payment. Remember, the calculator applies this payment on the next scheduled mortgage payment date after your chosen date.

- Refinance Options (Optional)

Explore if refinancing could be a viable strategy. This section is collapsed by default; click the header to expand it.

- New Interest Rate (%): The proposed interest rate for a new loan.

- New Loan Term (years): The proposed term for a new loan.

- Closing Costs: Any fees associated with originating the new refinance loan.

- Refinance Date: The date you anticipate closing on the new refinance loan.

- Action Buttons

- Calculate Payoff: Click this to process your inputs and display the results. A loading spinner will appear briefly.

- Reset: Clears all inputs and returns the calculator to its default settings.

Interpreting Your Results

Once you click “Calculate Payoff,” the “Your Payoff Report” section will appear, offering a comprehensive breakdown of your mortgage strategy and progress:

- Current Loan Progress: Shows your estimated percentage of principal paid so far, based on the current date. Also includes your current balance, total interest paid to date, and remaining interest — helping you understand where you stand today.

- Base Monthly EMI: Your original monthly mortgage payment, calculated without any extra contributions or changes to the payment schedule.

- Your Effective Payment: The actual amount you’ll pay monthly, factoring in any extra payments or biweekly strategy you’ve selected.

- Estimated Monthly Housing Cost: A broader view of your estimated total monthly housing expenses, including principal, interest, property taxes, homeowner’s insurance, and any additional fees (if provided).

- Original Payoff Date: The projected date your mortgage would have been paid off under the standard plan, with no accelerated strategies applied.

- New Accelerated Payoff Date: The updated, earlier payoff date reflecting your selected strategies — such as extra payments, biweekly schedules, or refinancing.

- Interest Breakdown: A detailed view of your interest costs, including total interest over the full loan term (based on your selected strategy), interest paid to date, and remaining interest still to be paid.

- Summary: A concise explanation of how much total interest you’ll save and how much sooner you’ll become mortgage-free compared to the original plan.

Tabs within Results:

- Strategies: A detailed comparison table of different payoff scenarios (baseline, biweekly, extra payments, lump sums, refinance) showing their respective payoff dates, total interest, and savings.

- Amortization: A full, detailed schedule of every payment, showing how much goes to principal and interest, and your remaining balance. This table reflects your accelerated strategy. Look for payments highlighted in blue; these are payments where a lump sum was applied.

- Charts: Visual representations of your loan balance over time and a comparison of total interest paid across scenarios.

- Timeline: A chronological view of key milestones in your mortgage journey.

Remember to use the Print Report button to save or print a PDF of your comprehensive report.

Comparison Table: Payoff Methods

Feature | Biweekly Payments | Extra Monthly Payments | Lump Sum Payments | Refinance |

How It Works | Half payment every 2 weeks (1 extra payment/year). | Add a fixed amount to your monthly payment. | One-time payment applied directly to principal. | Get a new loan with new rate/term to replace old one. |

Effort/Complexity | Low (automate with lender/bank). | Low (set up recurring transfer). | Moderate (requires available funds and planning). | High (application, closing, paperwork). |

Financial Impact | Modest savings, reduces term by a few years. | Significant savings, reduces term by several years. | Potentially large savings, immediate impact. | Potentially huge savings, can drastically change term. |

Flexibility | Low (fixed schedule). | High (can adjust amount or pause). | High (pay when funds are available). | Low (fixed new terms, requires commitment). |

Best For | Consistent income, wanting passive savings. | Consistent income, strong budgeting. | Unexpected windfalls, bonuses. | Lower rates available, desire for new term length. |

Drawbacks | May require manual setup if lender doesn’t support. | Discipline required to maintain. | Requires significant available cash. | Closing costs, extends total repayment period if not careful. |

Calculator Use | Check “Pay Biweekly” box. | Enter amount in “Extra Monthly Payment” field. | Use “Add Lump Sum Payment” and specify date/amount. | Input “New Interest Rate,” “New Loan Term,” “Closing Costs.” |

This table provides a quick overview, but remember to use the pay off mortgage faster calculator to see the exact numbers for your unique situation

Strategies for Faster Loan Payoff

Beyond understanding how the pay off mortgage faster calculator works, let’s explore some practical strategies you can implement to accelerate your mortgage payoff.

- The “Extra Payment” Power Play

Even a small, consistent extra payment can make a huge difference. Automate this. Set up a recurring transfer from your checking account to your mortgage principal each month. It’s painless and builds momentum.

- Example: If your mortgage payment is due on the 1st, set up an automatic transfer of an extra $50 (or $100, or whatever you can afford) to arrive a few days before your actual payment. Make sure to specify it’s for principal only.

- Harnessing the Biweekly Rhythm

If your lender allows it, switching to biweekly payments is a “set it and forget it” strategy that automatically funnels an extra month’s payment towards your principal each year.

- How to: Contact your lender to see if they offer a biweekly payment plan. If not, you can manually achieve the same effect by dividing your monthly payment by 12 and adding that amount to your regular monthly payment (e.g., if your payment is $1,200, pay an extra $100 each month).

- Strategic Lump Sum Application

Don’t let windfalls slip through your fingers! Tax refunds, work bonuses, inheritance, or even proceeds from selling unused items can be powerful tools.

- Best Practice: When you receive a lump sum, consider immediately applying it to your mortgage principal. Even a few thousand dollars can shave months off your loan and save significant interest. Use the pay off mortgage faster calculator to see the impact of different lump sum amounts and dates.

- Refinance Smartly

Refinancing isn’t just for lower interest rates. Consider a refinance to a shorter loan term (e.g., from 30 years to 15 years) if you can comfortably afford the higher monthly payments. While your monthly payment increases, you’ll pay substantially less interest over the life of the loan.

- When to Consider: When interest rates are significantly lower than your current rate, or if your financial situation has improved, allowing you to handle larger payments for a shorter term. Always factor in closing costs.

- The “Round Up” or “Round Down” Method

This is a playful way to find extra cash. If you pay bills online, round up your payment to the nearest $100. Or, if you get paid biweekly, round down your budgeted spending to leave a few extra dollars for your mortgage.

- Example: Your internet bill is $73. Instead of paying $73, pay $100 and allocate the extra $27 to your mortgage principal.

- The “Found Money” Approach

Dedicate any “found money” to your mortgage. This includes raises, tax refunds, bonuses, or even money saved from cutting out a discretionary expense (like that daily coffee, as our lifestyle savings option hints at!).

- Principal-Only Payments

When making extra payments, always ensure your lender applies the additional funds directly to your principal balance, not towards future interest or future monthly payments. Clearly mark “principal-only payment” on checks or specify it when paying online or over the phone.

By combining these strategies and using our pay off mortgage faster calculator to model their effects, you can craft a personalized plan to achieve mortgage freedom much sooner than you thought possible.

Want to explore ways to pay off your loan sooner? Use our Payoff Mortgage Faster Calculator to model different strategies.

Frequently Asked Questions (FAQs) About Pay off Mortgage Faster Calculator

Got questions about paying off your mortgage faster? We’ve got answers.

Does paying biweekly really save that much?

Yes! It might seem like a small change, but paying biweekly means you make 26 half-payments in a year. This is equivalent to 13 full monthly payments instead of 12. That one extra monthly payment per year goes directly towards your principal, significantly reducing your loan term and total interest paid over time. Our pay off mortgage faster calculator clearly demonstrates this.

Is paying off my mortgage early always worth it?

For most people, yes. It provides significant interest savings, builds equity faster, and offers immense psychological relief and financial flexibility. However, it’s not always the absolute best financial move for everyone. If you have high-interest debt (like credit cards) or high-return investment opportunities, those might offer a better “return” for your extra money. It’s a personal decision based on your risk tolerance, financial goals, and other debts.

What's the best strategy: extra payments, lump sum, or refinance?

There’s no single “best” strategy; the optimal approach depends on your individual circumstances.

- Extra monthly payments are great for consistent, gradual progress.

- Lump sums are powerful for one-time windfalls.

- Refinancing can be transformative if you can secure a significantly lower interest rate or a much shorter term. Often, a combination of these strategies yields the best results. Our pay off mortgage faster calculator allows you to mix and match to see which combination works for you.

How do I make sure my extra payments go to principal?

This is crucial! When making an extra payment, always explicitly instruct your lender that the additional funds should be applied to the principal balance. If paying online, look for an option like “principal-only payment.” If mailing a check, write “Apply to Principal” clearly in the memo line. If you don’t specify, the lender might hold the funds or apply them to your next standard payment, negating the benefit.

Will paying off my mortgage early affect my credit score?

Paying off your mortgage generally has a positive impact on your credit score over time, as it reduces your overall debt load and improves your debt-to-income ratio. Your credit history with a paid-off mortgage remains on your report for many years.

Should I pay off my mortgage or invest the money?

This is a classic financial dilemma.

- Paying off your mortgage offers a guaranteed return equal to your mortgage interest rate, tax-free (assuming no prepayment penalties). It’s a risk-free way to save money and gain peace of mind.

- Investing in the stock market (or other assets) could potentially offer higher returns than your mortgage interest rate, but it comes with risk and is not guaranteed. The choice depends on your risk tolerance, financial goals, and your mortgage interest rate. If your mortgage rate is high, paying it off might be more appealing. If it’s very low, investing might seem more attractive. A diversified approach, where you do a bit of both, is often recommended.

What are closing costs in a refinance, and do they matter?

Closing costs are fees charged by lenders and third parties for processing a new loan. They typically include appraisal fees, origination fees, title insurance, and more. Yes, they absolutely matter! These costs can be 2-5% of your loan amount. Our pay off mortgage faster calculator includes a field for closing costs so you can see their impact on your total interest and overall savings. You need to ensure the savings from a lower interest rate outweigh these upfront costs.

Glossary of Key Terms

Navigating mortgage terms can sometimes feel like learning a new language. Here’s a quick glossary to help you understand the key concepts discussed with our pay off mortgage faster calculator.

- Amortization: The process of paying off a debt over time through regular, scheduled payments. Early in the loan, more of your payment goes towards interest; later, more goes towards principal.

- Amortization Schedule: A table detailing each payment over the life of a loan, showing how much of each payment is applied to principal and interest, and the remaining balance.

- Annual Percentage Rate (APR): The annual rate charged for borrowing, expressed as a percentage. It includes the interest rate plus other costs, like certain fees, providing a more complete picture of the total cost of the loan.

- Biweekly Payments: Making half of your monthly mortgage payment every two weeks, resulting in 26 half-payments (or 13 full payments) per year.

- Closing Costs: Fees paid at the closing of a real estate transaction, typically including lender fees, title insurance, appraisal fees, and more.

- Equity: The portion of your home that you actually own. It’s calculated as your home’s market value minus your outstanding mortgage balance. As you pay down your principal, your equity increases.

- Escrow Account: An account held by your mortgage lender to pay property taxes and homeowner’s insurance on your behalf, typically funded by a portion of your monthly mortgage payment.

- Extra Monthly Payment: Any additional amount paid beyond your scheduled monthly mortgage payment, applied directly to the principal.

- Interest: The cost of borrowing money, expressed as a percentage of the loan amount.

- Interest Savings: The total amount of interest you avoid paying over the life of your loan by accelerating your payoff.

- Lump Sum Payment: A one-time, additional payment applied directly to your mortgage principal.

- Mortgage: A loan used to finance the purchase of a home.

- Principal: The original amount of money borrowed, or the remaining balance of the loan, on which interest is calculated. Paying down principal is key to saving interest and shortening your loan term.

- Private Mortgage Insurance (PMI): An insurance policy required by lenders for homebuyers who make a down payment of less than 20% of the home’s purchase price. It protects the lender, not the homeowner.

- Refinance: The process of paying off an old loan by taking out a new loan, typically with new terms (e.g., a lower interest rate or different loan term).

- Term (Loan Term): The duration, in years, over which you are scheduled to repay your mortgage.

Explore More Financial Tools

Our pay off mortgage faster calculator is just one of many tools designed to empower your financial journey. Discover other helpful calculators to manage your personal finances:

How Much House Can I Afford with My Income Calculator: Estimate how much home you can comfortably afford based on your monthly income, debts, and expenses—ideal for first-time buyers or those planning their next move.

- Amortization Chart Calculator: Get a detailed breakdown of your mortgage payments over time, showing principal and interest allocations for every single payment.

Ready to Own Your Home Sooner?

Don’t let your mortgage dictate your financial future. Take control today! Use our pay off mortgage faster calculator to experiment with different payment strategies and see exactly how much time and money you can save.

Calculate your path to freedom now! Explore the scenarios, export your personalized report to PDF, and share your findings with confidence. The first step to becoming mortgage-free starts here.

Need personalized advice? Consider speaking with a qualified financial advisor to discuss how these strategies fit into your broader financial plan.

Important Legal and Financial Disclaimer

The information and calculations provided by this pay off mortgage faster calculator are for illustrative and educational purposes only. They are based on the data you input and general mortgage principles.

This calculator is not financial advice. The results are estimates and may not reflect the exact figures provided by your mortgage lender. Actual interest charges, payment schedules, and payoff dates can vary due to factors such as:

- Your specific loan terms and conditions.

- The exact timing and processing of your payments.

- Any additional fees or charges not accounted for.

- Changes in interest rates (for adjustable-rate mortgages, which this calculator does not specifically model for future changes).

- Prepayment penalties (if applicable to your loan).

Before making any financial decisions, especially those involving significant sums like mortgage payments or refinancing, we strongly recommend:

- Consulting with a qualified financial advisor who can assess your personal financial situation and provide tailored advice.

- Contacting your mortgage lender directly to confirm current balances, payment application procedures, and any potential fees or penalties.