Mortgage Refinance Calculator – Cash-Out Refi, PMI, Tax Savings, Break Even & Comparison with Original Loan

Use this free home loan refinance calculator to estimate your savings. Compare cash-out or rate-term refi options against your current mortgage—PMI, breakeven, tax savings, and interest impact—secure, instant, and 100% browser-based with no sign-up or personal info required.

Please Note: The main calculation uses the 'New Interest Rate' as a fixed rate for the entire loan term. The ARM details are used to provide a risk warning in the results.

Introduction: Why Refinance Matters & How Our Mortgage Refinance Calculator Empowers You

In today’s dynamic financial landscape, homeowners are consistently looking for smarter ways to manage their most significant asset and debt: their home. The decision to refinance your mortgage is a momentous one, holding the potential to dramatically reshape your financial future – whether by reducing your monthly expenditures, gaining access to crucial cash from your home equity, or accelerating your journey towards financial freedom.

But how do you navigate the intricate world of interest rates, closing costs, and long-term implications to truly determine if a home loan refinance is the right move for you? This is precisely where our Advanced Mortgage Refinance Calculator comes in. Unlike many generic online tools that offer only basic payment estimates, our mortgage refinance calculator is meticulously engineered to provide a comprehensive, detailed, and truly personalized analysis. It’s more than just a simple refinance calculator; it’s a sophisticated financial modeling tool that puts you firmly in control.

We understand that you’re not merely searching for a single number; you’re seeking clarity. Our refinance mortgage calculator tackles the nuanced questions homeowners frequently ponder:

“How much will I truly save each month with a refinance savings calculator?”

“When will my savings actually outweigh the costs – what’s my precise mortgage refinance breakeven calculator point?”

“How do private mortgage insurance (PMI) and potential tax deductions, as calculated by a refinance tax benefit calculator, truly impact my real savings?”

“What if I want to use a cash-out refinance calculator to fund home improvements or consolidate debt, and how does that affect my mortgage cash out calculator calculations?”

“What are the specific implications for a second home loan refinance?”

Our mortgage refinance calculator seamlessly integrates all these critical factors, providing you with a complete financial picture.

We prioritize your privacy and ease of use above all else: no sign up is required, and absolutely no data is collected or stored. This commitment to privacy makes ours the best mortgage refinance calculator for users who value their financial confidentiality. You are empowered to run unlimited scenarios, confident that your financial information remains yours alone. This home loan refinance calculator is your trusted partner.

This comprehensive guide will walk you through every feature of our advanced mortgage refinance calculator, show you precisely how to interpret its detailed results, and provide real-world examples to illustrate its immense power. Dive in to unlock deep insights into your potential mortgage refinance savings and gain the confidence to make the best decision for your financial future.

Understanding Mortgage Refinancing: The Core Concepts

At its heart, mortgage refinancing means replacing your existing home loan with a brand new one. It’s essentially taking out a new loan to pay off your previous one, initiating a fresh lending process complete with new terms, rates, and associated closing costs, much like your original home purchase. This fundamental concept implies a full financial reset for your home debt.

Homeowners typically engage in mortgage refinance for various strategic reasons, often driven by a desire to align their home loan with current market conditions or evolving personal financial goals. Common objectives include:

Securing a lower interest rate: This directly reduces your monthly payments, freeing up cash flow.

Opting for a shorter loan term: This accelerates debt payoff and leads to significant savings on total interest paid over the life of the loan.

Undertaking a cash-out refinance: This allows you to access accumulated home equity. This equity can be strategically used for crucial purposes such as high-interest debt consolidation, funding significant home improvements, or covering major expenses like higher education.

Beyond these primary drivers, a refinance can also offer benefits like eliminating Private Mortgage Insurance (PMI) once sufficient equity is built, or switching between adjustable-rate and fixed-rate mortgage types for greater payment stability or initial savings.

Understanding these core motivations is the first step in deciding if a refinance mortgage calculator analysis is right for you. Our mortgage refinance calculator is specifically built to illuminate these possibilities, helping you analyze the nuanced financial implications of each potential choice. This home loan refinance calculator provides crucial clarity.

How Our Advanced Mortgage Refinance Calculator Works: A Step-by-Step Guide

Our goal is to transform a complex financial decision into a clear and actionable process. The Advanced Mortgage Refinance Calculator is designed with an intuitive interface, enabling you to effortlessly input your specific financial details and instantly observe powerful results. Follow these steps to harness its full potential and leverage its capabilities as a comprehensive refinance calculator:

Step 1: Input Your Current Mortgage Details

This section establishes the baseline for comparison, providing the mortgage refinance calculator with your existing loan information.

Original Loan Amount ($): Enter the initial principal amount of your current mortgage.

Current Interest Rate (%): Input your existing annual interest rate on your home loan.

Original Loan Term (Years): Specify the initial length of your mortgage in years (e.g., 30 years, 15 years).

Start Date of Loan: This date is absolutely crucial for our mortgage refinance calculator to accurately determine your current remaining balance. Our calculator uses this date along with your original terms to precisely compute how much principal you’ve already paid down.

Remaining Term (Years) (Optional): If you happen to know the exact remaining years on your loan, you can enter it here to override the auto-calculated value. Otherwise, leave this field blank, and the calculator will derive it automatically. This makes our home loan refinance calculator highly adaptable.

Step 2: Define Your Refinance Type

This critical choice dictates additional relevant inputs and shapes the calculations performed by the refinance calculator.

Rate & Term: Select this option if your primary objective is to lower your interest rate or change your loan term without taking out any extra cash. This is the most common use case for a refinance mortgage calculator.

Cash-Out: Choose this if you intend to borrow against your accumulated home equity to receive a lump sum of cash.

Cash-Out Amount ($): (This field will only appear if “Cash-Out” is selected). Specify the exact amount of cash you wish to receive. Our integrated cash-out refinance calculator feature will factor this amount directly into your new loan principal.

Current Home Value ($): (This field will also only appear if “Cash-Out” is selected). Input your home’s estimated current market value. This information is vital for calculating your Loan-to-Value (LTV) ratio, which can significantly impact lending terms and the need for PMI.

Step 3: Enter Your New Mortgage Details

This section defines the precise terms of your prospective refinance loan, allowing the mortgage refinance calculator to project your future payments.

New Interest Rate (%): Input the estimated interest rate you anticipate securing for your new loan. Our mortgage refinance rates calculator capability uses this rate for all forward-looking financial projections.

New Loan Term (Years): Specify the desired length of your new mortgage in years (e.g., 15, 20, or 30 years).

New Loan Start Date: This is the anticipated date when your new refinanced loan would officially begin.

New Mortgage Principal (Auto Calculated): This dynamic display shows the estimated principal for your new loan. It automatically combines your remaining balance from the old loan, any cash-out refinance amount you specified, and any closing costs you opt to roll into the loan.

Manually override new principal: Check this box if you have a very specific target loan amount in mind for your new mortgage, giving you direct control over this figure.

Custom New Principal Amount ($): (This field will only appear if the override checkbox is selected). Enter your precise desired new principal amount.

Loan Type:

Fixed Rate: Select this for predictable, stable payments throughout the entire loan term.

Adjustable-Rate (ARM): While our primary calculations use a fixed rate for simplicity in forecasting payments, selecting ARM allows you to input “Initial Fixed Period,” “Adjustment Frequency,” “Adjustment Cap,” and “Max Lifetime Rate” for your informational guidance. A clear note will appear reminding you that the main payment calculation will still use the initial ‘New Interest Rate’ as a fixed rate for the full term.

Step 4: Account for Closing Costs & Fees (Expand Accordion)

Closing costs can significantly impact your mortgage refinance breakeven calculator results. This expandable accordion allows you to detail these crucial expenses, making your refinance closing costs calculator analysis highly accurate.

Estimated Closing Costs ($): Input the total estimated fees from your lender and any third parties involved in the transaction (e.g., appraisal, origination, title insurance). Our refinance closing costs calculator element will use this figure in its comprehensive calculations.

Roll costs into loan?: Decide whether to finance these costs directly into your new mortgage or pay them upfront out-of-pocket. This crucial choice impacts your new principal amount and directly influences your breakeven point.

Prepayment Penalty ($): If your current loan agreement includes a penalty for early payoff, enter that amount here. This fee is typically treated as an upfront cost in our calculations.

Other Fees (Escrow, Title, etc.) ($): Account for any additional costs associated with the refinance transaction that aren’t covered by estimated closing costs.

Step 5: Utilize Advanced Settings (Expand Accordion)

These optional but highly impact full settings allow for a much more precise analysis, transforming our tool into a truly advanced mortgage refinance calculator.

Current Home Value ($): This value is used for Loan-to-Value (LTV) calculations relevant to PMI, and for estimating property tax and home insurance. If you selected the “Cash-Out” option earlier, this value will automatically carry over.

Manually specify PMI: Check this option to enter your exact Private Mortgage Insurance details, either as an annual percentage of the loan amount or a fixed monthly amount. This will override the calculator’s default PMI logic. Our refinance with PMI calculator feature becomes highly customizable here.

Property Tax (Annual): Input your annual property tax. You have the flexibility to enter it either as a percentage of your home’s value or as a fixed dollar amount.

Home Insurance (Annual): Input your annual homeowner’s insurance premium. Similar to property tax, you can enter this as a percentage of home value or a fixed dollar amount.

HOA Fees (Monthly $): Enter your monthly Homeowners Association fees, if applicable to your property.

Tax Settings (appears for US country selection): These settings are crucial for leveraging the refinance tax benefit calculator aspects of our tool.

Country: Currently set to “United States” for tax calculations.

Do you itemize deductions?: This selection directly affects your eligibility for the mortgage interest deduction.

Filing Status: Your tax filing status (e.g., Single / Married Filing Jointly, Married Filing Separately) impacts specific deduction limits.

Original mortgage from before Dec 16, 2017: This is crucial for applying the correct federal mortgage interest deduction limits, as tax laws changed.

Federal tax bracket: Select your marginal federal income tax bracket. This is the rate at which your next dollar of income would be taxed, directly influencing your tax savings from mortgage interest.

I live in a high-tax state: A checkbox to account for additional tax considerations and potential increased federal deduction value in states with high income taxes.

Step 6: Calculate and Interpret Your Results

Once all relevant fields are accurately filled, click the “Calculate” button. The results section will instantly populate with a comprehensive report. We’ll detail how to interpret these powerful results in the very next section, helping you understand your refinance savings. This is where our home loan refinance calculator truly shines.

Need to adjust your details?

Just scroll up and tweak your inputs. Our free, secure refinance calculator updates your breakeven, PMI, tax impact, and savings in real time.

Interpreting Your Results: Unlocking Deep Refinance Insights

Once you click “Calculate,” our Advanced Mortgage Refinance Calculator meticulously processes your inputs and presents a comprehensive, easy-to-understand report. This isn’t just a basic summary; it’s a detailed breakdown meticulously designed to help you make truly informed decisions about your home loan refinance.

1. Recommendation Summary: Your Quick Guide

At the very top of the results, you’ll find a concise “Recommendation Summary”. This immediate assessment provides a quick, color-coded snapshot of your refinance scenario’s overall financial health:

“Good Move!”: This indicates that your refinance is highly likely to provide significant financial benefits, such as substantial monthly savings or a notable reduction in future interest paid.

“Consider Carefully”: This suggests that while there are benefits, trade-offs also exist. For example, you might experience monthly savings but potentially pay more interest over the long term, or vice versa. This assessment often appears with cash-out refinance calculator scenarios where monthly payments might rise but are offset by the elimination of high-interest debt.

“Not Recommended”: This indicates that the proposed mortgage refinance is likely to be more expensive overall, either on a monthly basis or in total interest paid, thus outweighing any potential benefits.

This summary is your initial, clear indication of whether your specific home loan refinance scenario aligns with common financial goals.

2. Key Financial Impact: Your Most Important Metrics

This section highlights the most critical figures for your refinance decision, offering the core insights of a refinance savings calculator:

Monthly Savings: This represents the immediate change in your total estimated monthly payment (which includes Principal, Interest, Property Tax, Home Insurance, and HOA fees). A positive number means you save money each month, directly improving your cash flow. A negative number indicates an increased monthly payment. This is a core output for anyone using a mortgage refinance calculator to reduce payments.

Future Interest Saved: This crucial figure represents the total amount of interest you could save over the remaining term of your original loan path, compared to the total interest (including PMI, if applicable) on your new refinanced loan. A positive number indicates significant long-term interest savings. This helps you calculate true mortgage refinance savings over the long haul.

Breakeven Point: This is a crucial output from our embedded mortgage refinance breakeven calculator. It tells you precisely how long (in months and an estimated date) it will take for your accumulated monthly savings to offset the total costs of refinancing (such as closing costs, prepayment penalties, etc.). If you plan to sell your home before reaching this point, the refinance might not be financially sound.

Loan Term Impact: This concisely shows whether your new refinance shortens or extends your overall loan payoff date compared to your original mortgage’s projected end. It also clearly displays your new projected payoff date.

3. Current Mortgage Progress: Visualizing Your Equity

This section provides a clear visual and numerical representation of your current home loan status, offering insights typically found in an equity calculator:

Progress Bar: A dynamic bar visually shows the percentage of principal you’ve already paid off on your original loan.

Principal Paid: The total amount of principal you’ve paid to date on your existing mortgage.

Remaining Balance: The outstanding principal balance on your current loan as of the refinance start date. This is the essential starting point for your new refinance.

Equity Position: The percentage of your home’s value that you own outright (calculated based on principal paid relative to the original loan amount and your current home value).

4. Refinance Details: A Granular Breakdown

This detailed grid offers a more granular look at the financial components of your refinance, providing specifics beyond what a basic refinance calculator might offer:

Balance at Refinance: Your outstanding principal on the old loan.

% Principal Paid (Original): The percentage of your original loan amount that you’ve already paid down.

Original Monthly P&I vs. New Monthly P&I Payment: A direct comparison of just the principal and interest portions of your payments.

Total Closing Costs: The sum of all estimated fees for your new loan. This figure is directly informed by our refinance closing costs calculator logic.

Total Upfront Cash Required: The amount you’ll need to pay out-of-pocket at closing (if you choose not to roll costs into the loan, plus any prepayment penalty).

Total Interest (New Mortgage Only): The estimated total interest you will pay over the full term of your new refinanced mortgage.

Lifetime Interest (Original + New): This is a crucial long-term metric. It shows the cumulative interest you will have paid from the very beginning of your original loan up to the projected payoff date of your new refinanced loan. It compares this figure against the original loan’s full lifetime interest, helping you see the true long-term financial impact.

PMI Status for New Mortgage: Indicates if Private Mortgage Insurance is applicable, its monthly cost, and when it’s estimated to be removed (if applicable). This is a key output for a refinance with PMI calculator.

New Mortgage-to-Value (LTV): Your Loan-to-Value ratio for the new loan, calculated as (New Principal / Current Home Value) * 100. This is especially important for cash-out refinance calculator scenarios and PMI considerations.

5. Tax Considerations: Boosting Your Savings (for US Residents)

If you indicated that you itemize deductions and live in the U.S., this section, powered by our refinance tax benefit calculator, provides powerful insights into potential tax benefits:

Est. Monthly Tax Savings (Year 1 Only): An estimated amount you could save each month on your federal taxes specifically due to the mortgage interest deduction. This is based on the interest paid in the first year of the new loan and your specified tax bracket and filing status.

Effective Interest Rate (After Tax): This is your nominal new interest rate adjusted to account for the tax savings you receive from the mortgage interest deduction. It represents your true cost of borrowing after considering this federal benefit.

6. Detailed Insights: Tabs for Deeper Analysis

The results are further organized into intuitive tabs for deeper dives, providing a comprehensive view of your mortgage refinance:

Strategies Tab: Provides a concise table comparing your “Current Loan” and “New Loan” side-by-side for key metrics such as monthly payment, remaining interest paid, and loan payoff date. This helps you quickly assess the overall impact of your home loan refinance.

Amortization Tab: Offers a full, month-by-month amortization schedule for your new loan. This detailed table shows precisely how each of your new payments is broken down into principal, interest, PMI (if applicable), and estimated property tax/insurance/HOA, along with the declining balance. It’s a transparent view of your debt repayment.

Charts Tab: Visualizes your financial journey with two powerful graphs:

Mortgage Balance Over Time: A clear line chart comparing the projected remaining balance of your original mortgage (had you not refinanced) against the new refinance loan’s balance. It clearly shows how your new loan performs over time and includes a crucial annotation for your breakeven point.

Total Interest Paid Comparison: A bar chart illustrating the total interest paid for the remaining term of your original loan versus the total interest for your new refinanced loan. This visual quickly highlights potential long-term interest savings.

Timeline Tab: Presents key financial milestones on an easy-to-read chronological timeline. This includes your original loan start, refinance start, original payoff date, new payoff date, your calculated breakeven point, and your estimated PMI cancellation date.

Feature Highlights: Why Our Mortgage Refinance Calculator Stands Out

You might be asking, “Why use this mortgage refinance calculator when there are so many others available online?” The truth is, not all calculators are created equal. Many provide only surface-level estimates, often leaving you with more questions than answers. Our Advanced Mortgage Refinance Calculator is meticulously engineered to provide unparalleled depth and accuracy, setting it significantly apart from typical tools. We firmly believe in empowering you with comprehensive financial insights, not just simple numbers. Here’s what makes our home loan refinance calculator truly superior, addressing key aspects that often go unaddressed by basic online alternatives:

The following table, compare this calculator:

Feature | Our Calculator | Typical Online Tools |

Breakeven Point Analysis | ✅ Yes (Precise date & duration based on all costs & savings) | ❌ No / Limited (often just total cost without time) |

PMI Calculation & Removal Logic | ✅ Yes (Auto-calculated, allows override, estimates cancellation month) | ❌ No / Basic only (may ask if you have PMI, but not calculate) |

Cash-Out Refinance Option | ✅ Yes (Accurately calculates new principal with cash-out & rolled costs) | ❌ No / Limited (rarely integrates cash-out into principal) |

Tax Deduction Simulation | ✅ Yes (Federal, considers loan date, filing status, tax bracket, high-tax state impact) | ❌ No / Very Basic (if at all, often just a generic disclaimer) |

Interactive Visual Charts | ✅ Yes (Dynamic balance and interest charts, breakeven annotations) | ❌ No / Static or Limited (simple graphs without deep insights) |

Amortization Schedule | ✅ Yes (Detailed month-by-month breakdown of P, I, PMI, Tax/Ins/HOA) | ❌ No / Summary only (provides total interest, not per payment) |

Loan Term Impact Analysis | ✅ Yes (Clearly compares old vs. new payoff dates and duration change) | ❌ No (focuses only on new term) |

Privacy Guaranteed | ✅ Yes (No signup, no data collected or stored) | ❌ Often requires email/personal info to deliver results |

Comprehensive Tooltips | ✅ Yes (Contextual help for every input field) | ❌ No / Minimal (leaves users guessing) |

Printable Report | ✅ Yes (Detailed, PDF-friendly summary of all results) | ❌ No |

Let’s delve deeper into some of these differentiating features, which make ours the best mortgage refinance calculator available:

Unparalleled Breakeven Point Precision Our mortgage refinance breakeven calculator is not just a theoretical figure. It precisely calculates the exact number of months required for your cumulative monthly savings to offset all your refinance-related costs, including closing costs (whether paid upfront or rolled in) and any applicable prepayment penalties. This granular detail ensures you know exactly when your refinance truly begins to pay off. This is a critical factor often overlooked by basic refinance calculators.

Intelligent PMI Logic Private Mortgage Insurance (PMI) can add a significant cost to your monthly payment. Our refinance with PMI calculator dynamically assesses if PMI is applicable based on your Loan-to-Value (LTV) ratio for the new loan. Beyond just calculating the monthly PMI, it also estimates the precise month your PMI can be canceled based on reaching a 78% LTV, providing a clear future financial milestone. You even have the option to manually override the PMI rate or amount if you have specific policy details. This level of detail goes far beyond what a standard home loan refinance calculator typically offers.

Sophisticated Tax Deduction Simulation For U.S. homeowners who itemize deductions, the mortgage interest deduction can provide substantial tax savings. Our mortgage refinance calculator uniquely integrates federal tax law nuances, considering your specific tax bracket, filing status (e.g., Married Filing Separately), whether your original mortgage predates the 2017 tax law changes (which affected deduction limits), and even the impact of living in a high-tax state. This helps you understand your “Effective Interest Rate” post-tax, giving you a truer picture of your borrowing cost and making it a powerful refinance tax savings calculator.

Transparent Cash-Out Principal Calculation When you utilize our mortgage cash out calculator feature, you get a clear breakdown of precisely how your new mortgage principal is formed – starting from your remaining balance, adding your desired cash-out amount, and then incorporating any rolled-in closing costs. This level of transparency is rare among typical cash-out refinance calculators and is crucial for understanding your total new debt burden.

Unwavering Privacy Assurance In an age where personal data is constantly sought, we stand firm on our unwavering commitment to your privacy. This mortgage refinance calculator operates entirely within your web browser. We do not collect, store, or transmit any of your personal financial data. You can confidently explore unlimited “what-if” scenarios without any risk to your information. This makes it the best mortgage refinance calculator for privacy-conscious users.

Our comprehensive suite of features ensures that whether you’re performing a quick “should I refinance my mortgage calculator” check or a deep dive into your second home loan refinance options, you have all the tools for a truly insightful analysis. This home loan refinance calculator is designed to meet your every need.

Start Your Advanced Refinance Analysis Now!

Example Scenarios: Real-World Applications of Our Mortgage Refinance Calculator

Seeing is believing. Let’s explore how real people, with real questions, can use our Advanced Mortgage Refinance Calculator to find answers and make informed decisions. These scenarios highlight the versatility of our home loan refinance calculator for achieving various financial goals.

Scenario 1: Lowering the Monthly Payment (Rate & Term Refinance)

Goal: Refinance an existing mortgage into a new loan with a lower interest rate to reduce monthly expenses.

Inputs:

- Original Loan: $300,000 at 6.5% (30-year fixed), initiated August 2022

- New Loan: Remaining balance refinanced into a new 30-year loan at 5.5%

- Closing Costs: $5,000 (rolled into the new loan)

Calculated Results:

- Recommendation Summary: ✅ Good Move!

- This refinance improves monthly cash flow and leads to a total interest savings of $17,907 compared to continuing with the existing loan.

Key Financial Impact:

- Monthly Mortgage Change : -$225.48

- Future Interest Saved: $17,907

- Breakeven Point: June,2027 (22 months-time needed for monthly savings to offset closing costs)

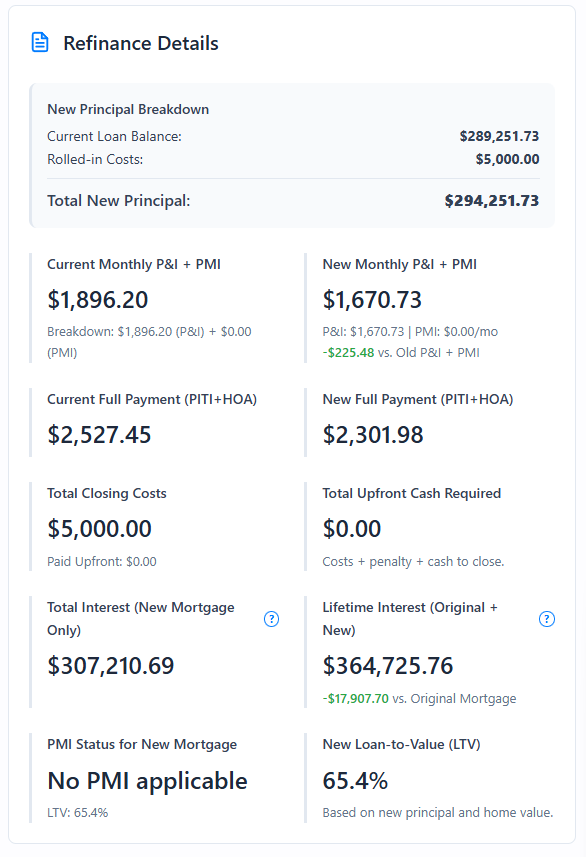

Refinance Details:

- Current Monthly P&I: $1,896.20

- New Monthly P&I: $1,670.73

- Remaining Balance: $289,251.73

- New Principal (with costs): $294,251.73

Calculator result showing the financial impact of refinancing a $300,000 loan from 6.5% to 5.5%, including breakeven timeline and interest savings.

Key Takeaway: The 22-month breakeven point is the most critical insight. Monthly savings are only meaningful if the homeowner remains in the property beyond this period. If sold earlier, the upfront costs could outweigh the benefits. This refinance makes financial sense primarily for those planning to stay put for several more years.

Scenario 2: Consolidating Debt (Cash-Out Refinance)

Goal:

Access home equity to pay off high-interest debt, streamline finances into one mortgage payment, and improve monthly cash flow.

Inputs:

- Original Loan: $350,000 at 6.0% (30-year fixed), initiated August 2020

- Home Value: $500,000

- Cash-Out Amount: $40,000

- New Loan: Balance + cash-out refinanced into new 30-year loan at 5.75%

- Closing Costs: $6,000 (rolled into loan)

- Monthly Debts Eliminated: $750 (credit card, auto loan, etc.)

Calculated Results:

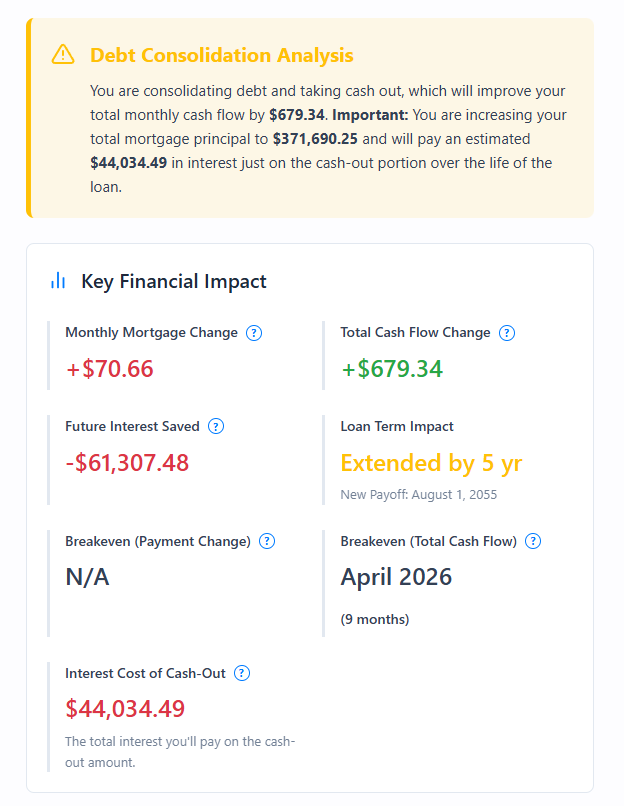

- Recommendation Summary:

Debt Consolidation Analysis

Debt Consolidation Analysis - While the mortgage payment increases slightly, total monthly outflows are reduced, improving cash flow and simplifying debt structure.

Key Financial Impact:

- Mortgage Payment Change: +$70.66 (increase in monthly mortgage payment)

- Net Cash Flow Change: +$679.34 (total monthly savings after eliminating old debts)

- Breakeven Point (Cash Flow): 9 months

- Interest Cost of Cash-Out: $44,034.49 (interest paid on $40,000 over the full loan term)

Refinance Details:

- New Principal (with cash out & costs): $371,690.25

- New Loan-to-Value (LTV): 74.3%

Screenshot of calculator output displaying a “Debt Consolidation Analysis” summary with a cash-out amount, interest cost of $44,034.49, and net cash flow improvement of $679.34 per month.

Key Takeaway: This approach trades short-term financial relief for long-term cost. The key number is the $43,034.49 interest cost of extracting equity. While not optimal for minimizing total interest, it can be worthwhile for someone needing breathing room in their monthly budget. The decision hinges on whether the immediate approximate $700/month benefit justifies the lifetime cost of repackaging the debt.

Scenario 3: Paying Off the Loan Faster (Strategic Payoff Refinance)

Goal: Reduce total interest paid and shorten the loan term by refinancing into a shorter duration with a lower rate, even if the monthly payment increases.

Inputs:

- Original Loan: $400,000 at 6.25% (30-year fixed), initiated August 2019

- New Loan: Remaining balance refinanced into a 15-year loan at 5.25%

- Closing Costs: $4,000 (paid out-of-pocket)

- Home Value (Advanced Settings): $450,000

Calculated Results:

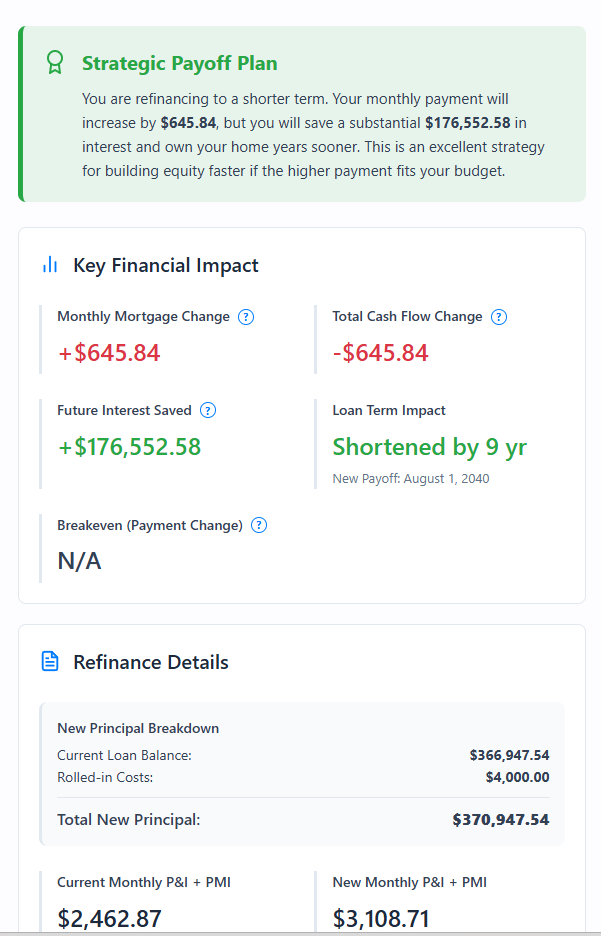

- Recommendation Summary:

Strategic Payoff Plan

Strategic Payoff Plan - This strategy significantly accelerates equity building and delivers massive long-term savings.

Key Financial Impact:

- Monthly Payment Change: +$645.84 (higher monthly outflow due to shorter term)

- Future Interest Saved: $176,552.58

- Loan Term Reduced By: 9 years

Refinance Details:

- Current Monthly P&I: $2,462.87

- New Monthly P&I: $3,108.71 (New P&I = $2,981.97 + New PMI = $126.74)

- New Payoff Date: August 2040 (instead of August 2049)

Screenshot showing refinance results with a “Strategic Payoff Plan” summary, $176,552 saved in interest, shortened loan term by 9 years, and increased monthly payment to $3,108.71.

Key Takeaway: This is a proactive wealth-building strategy. The higher payment today leads to $176,552 in interest savings and a faster debt-free milestone. Viewed properly, it’s not just a payment—it’s an investment in long-term financial freedom and asset ownership. This approach works best for those with strong, stable income and a long-term residence plan.

Should You Refinance? Pros & Considerations

Our Advanced Mortgage Refinance Calculator provides you with all the essential data, but the ultimate decision to refinance is yours alone. Understanding the overarching benefits and important considerations is key to determining if a home loan refinance truly aligns with your personal financial strategy.

✅ Benefits of Refinancing

- Lower Interest Rate or Shorter Term: This is often the primary driver for a mortgage refinance. A lower interest rate directly reduces your monthly payment and the total interest you’ll pay over time. A shorter loan term means a faster payoff and significant interest savings over the life of the loan. Our mortgage refinance rates calculator helps you pinpoint this.

- Eliminate Private Mortgage Insurance (PMI): If your home equity has grown to 20% or more (translating to an 80% LTV), refinancing can allow you to drop PMI, which is an additional monthly cost on your loan. Our calculator’s PMI logic helps you determine this.

- Tap Home Equity for Needs: A cash-out refinance allows you to convert a portion of your home equity into liquid cash. This can be a smart way to fund major home improvements, consolidate high-interest debt (like credit cards), pay for education, or make other significant investments, often at a lower interest rate than other loan types. Our cash-out refinance calculator feature helps you model these scenarios.

- Simplify Multiple Debts: By consolidating higher-interest debts into a single, lower-interest home loan refinance, you can streamline your monthly payments and potentially reduce your overall debt burden. This home loan refinance calculator will show you the impact.

- Switch Loan Types: Transitioning from an Adjustable-Rate Mortgage (ARM) to a Fixed-Rate Mortgage can provide enhanced payment stability and predictability, protecting you from future rate increases.

⚠️ Important Considerations

- Closing Costs: Refinancing is never free. You will incur closing costs, which can range from 2% to 5% of the loan amount. While you can often roll these into your new loan, they still add to your total debt. Our refinance closing costs calculator element is crucial for this assessment.

- Breakeven Time: This is paramount for any refinance decision. You need to stay in your home long enough for the monthly savings to recoup the costs of refinancing. If your breakeven point is, for instance, 4 years, but you plan to move in 2 years, refinancing might not be financially sound. Our mortgage refinance breakeven calculator is designed to give you this critical insight.

- Higher Long-Term Interest (if resetting term): If you refinance an existing loan with 20 years left into a new 30-year loan (even at a lower rate), you might save monthly but pay more total interest over the lifetime of the loan because you’re extending the repayment period.

- PMI Might Restart (if equity <20%): If your current LTV is already below 80% but your new refinance loan brings it back above that threshold (e.g., with a cash-out refinance), you might find yourself paying PMI again. The calculator helps you foresee this.

- Credit Score Impact: The application process involves a hard credit inquiry, which can temporarily ding your score. Repeated refinance applications in a short period could cumulatively affect your credit.

- Loss of Unique Loan Features: Some government-backed loans (FHA, VA, USDA) have unique benefits that may be lost if you refinance into a conventional loan.

Using our mortgage refinance calculator allows you to carefully weigh these pros and cons against your personal financial situation and goals.

References Used to Build This Calculator

These reputable sources provide foundational information and official guidelines related to mortgage refinancing and home loans.

This refinance calculator is developed using trusted sources to ensure financial accuracy and transparency. The following references informed the core logic behind breakeven analysis, PMI modeling, tax benefits, and cost structure:

🔹 IRS – Publication 936: Home Mortgage Interest Deduction

Authoritative IRS guidance on how mortgage interest and discount points can be tax-deductible — used in modeling effective interest rates and tax savings.

🔹 Consumer Financial Protection Bureau (CFPB) – Loan Estimate & Closing Disclosure

Outlines what borrowers should expect regarding closing costs, loan terms, and disclosures — directly influencing the structure of this calculator’s cost inputs.

🔹 Investopedia – Cash-Out Refinance

Provides insights into how cash-out refinancing works, its pros/cons, and how it impacts home equity — reflected in the cash-out modeling section of the tool.

🔹 Wikipedia – Loan-to-Value (LTV) Ratio

Explains LTV’s importance in mortgage approvals, PMI eligibility, and cash-out limitations — applied to our equity and risk warnings.

🔹 Wikipedia – Debt-to-Income (DTI) Ratio

Covers how lenders evaluate your ability to afford the new loan — a factor considered when showing cash flow changes and affordability after refinancing

Explore More Financial Tools

Expand your financial knowledge with our other helpful tools:

- Curious about how much house you can truly afford? Use our How Much House Can I Afford Calculator to align your homeownership dreams with your financial reality.

- Want to see a detailed breakdown of your mortgage payments over time? Explore our Comprehensive Amortization Chart Calculator to visualize your principal and interest payments for any loan.

Frequently Asked Questions (FAQs) About Mortgage Refinance Calculators

We’ve compiled answers to the most common questions homeowners have when considering a mortgage refinance, drawing on common online search queries and user concerns.

What's the "breakeven point" and why does it matter for my mortgage refinance?

The breakeven point is the amount of time (in months or years) it takes for your cumulative monthly savings from refinancing to equal the total costs associated with the refinance (closing costs, prepayment penalties, and other fees). It matters because if you sell your home before reaching this point, you might end up spending more on the refinance than you save. Our refinance breakeven point calculator feature precisely calculates this for you, helping you determine if a refinance is financially sound given your expected time in the home.

Should I roll my closing costs into the loan or pay them upfront?

This depends heavily on your cash availability and long-term goals.

- Rolling costs into the loan: Means you don’t pay out-of-pocket at closing, but your new loan principal increases, leading to more total interest paid over the life of the loan. This also extends your breakeven point. This is a common choice if you have limited immediate cash.

- Paying costs upfront: Reduces your new loan principal, which means less total interest paid over time. It also shortens your breakeven point. This is generally recommended if you have the funds available.

Our refinance closing costs calculator functionality allows you to model both scenarios.

Will I pay more interest if I refinance to a longer term, even with a lower rate?

Possibly, yes. If you refinance a loan with, say, 20 years remaining into a new 30-year home loan, even at a lower interest rate, you are extending the overall repayment period. This often results in paying more total interest over the lifetime of the loan, despite potentially enjoying lower monthly payments. Our mortgage refinance calculator explicitly shows the “Lifetime Interest (Original + New)” comparison, helping you fully understand this crucial trade-off.

How does a cash-out refinance affect my home equity?

A cash-out refinance converts a portion of your home equity into liquid cash by taking out a larger home loan. While it provides immediate funds, it inherently reduces your immediate equity in the home because your loan principal increases. Your Loan-to-Value (LTV) ratio will increase. Our cash-out refinance calculator feature clearly illustrates this impact on your new principal and LTV.

When does PMI get removed after refinancing?

If your new home loan requires Private Mortgage Insurance (PMI) because your Loan-to-Value (LTV) is above 80%, you can typically request its cancellation once your principal balance drops to 80% of your home’s original appraised value. PMI typically automatically terminates when your loan balance reaches 78% of the original value. Our advanced mortgage refinance calculator estimates your PMI cancellation month, helping you anticipate when this monthly cost will disappear.

Are refinance costs tax deductible?

Some refinance costs, specifically “points” (loan origination fees), may be deductible as prepaid interest over the life of the loan. Other closing costs (like appraisal fees, title fees, attorney fees) are generally not deductible but can be added to your home’s basis, which might reduce capital gains if you sell the home later. Mortgage interest itself remains deductible if you itemize. Always consult a tax professional for personalized advice, as tax laws are complex. Our calculator includes a “Tax Considerations” section for estimated federal mortgage interest deduction benefits.

What is an "effective interest rate" and why does it matter?

Your “effective interest rate” is your nominal interest rate on the mortgage, specifically adjusted to account for the tax savings you receive from deducting mortgage interest. It provides a more accurate picture of your true cost of borrowing. If you itemize deductions and are in a certain tax bracket, your effective interest rate will be lower than your nominal rate. Our advanced mortgage refinance calculator provides this metric, particularly useful for US homeowners.

How often can I refinance my mortgage?

There’s no legal limit to how many times you can refinance. However, each refinance incurs new closing costs. It’s usually only advisable to refinance if the savings outweigh these costs (i.e., you reach your breakeven point) within a reasonable timeframe that aligns with your plans to stay in the home. Constantly refinancing may also temporarily impact your credit score due to multiple hard inquiries.

What documents will I need for a refinance application?

You’ll typically need to provide proof of income (pay stubs, W-2s, W-2s, tax returns), asset statements (bank accounts, investment accounts), debt statements (current mortgage, credit cards, auto loans), and property documents (tax bill, insurance declarations). Be prepared to provide at least two years of financial history to your lender.

Glossary of Essential Mortgage Refinance Terms

Navigating the world of home loan refinance can often introduce a new vocabulary. Here’s a comprehensive glossary of key terms used by our Advanced Mortgage Refinance Calculator and commonly found throughout the refinance industry:

- Amortization: The systematic process of paying off a debt over time in regular, scheduled installments, where each payment covers both a portion of the principal and the accrued interest. Our calculator provides a detailed amortization chart calculator output.

- Appraisal: An unbiased, professional assessment of a property’s current market value, typically required by lenders to ensure that the loan amount is justified by the home’s market value.

- APR (Annual Percentage Rate): The total cost of a loan over its full term, expressed as a yearly rate. It includes the interest rate plus certain fees and points, providing a more comprehensive measure of the loan’s cost than the interest rate alone.

- Breakeven Period: The precise amount of time (in months or years) it takes for the monthly savings generated from a refinance to fully cover the total costs associated with the refinance. A key output from our refinance breakeven point calculator.

- Cash-Out Refinance: A specific type of home loan refinance where you replace your existing mortgage with a larger one and receive the difference in cash, typically for debt consolidation or home improvements.

- Closing Costs: Various fees and expenses incurred during the process of taking out a new mortgage loan. These can include appraisal fees, origination fees, title insurance, and more. Our refinance closing costs calculator considers these.

- Debt-to-Income (DTI) Ratio: A financial ratio that directly compares your total monthly debt payments to your gross monthly income. Lenders use it to assess your ability to manage monthly payments and repay debt.

- Effective Interest Rate: Your nominal mortgage interest rate adjusted to reflect the tax savings from the mortgage interest deduction (for those who itemize). Our advanced mortgage refinance calculator provides this.

- Escrow: An account held by a neutral third party (often the lender or a servicing company) where funds for property taxes and homeowner’s insurance are collected with your monthly mortgage payment and paid out when due.

- Home Equity: The portion of your home’s current value that you own outright. Calculated as the current market value of your home minus your outstanding mortgage balance.

- Interest Rate: The percentage charged by the lender for the money you borrow, expressed as an annual percentage of the outstanding loan balance.

- Loan-to-Value (LTV) Ratio: A financial ratio widely used by lenders to assess lending risk. It compares the amount of your mortgage loan to the appraised value of the property. For example, a $200,000 loan on a $250,000 home has an 80% LTV.

- Origination Fee: A fee specifically charged by the lender for processing a loan application. It is often expressed as a percentage of the loan amount, commonly referred to as “points”.

- PMI (Private Mortgage Insurance): An insurance policy that specifically protects the lender (not the borrower) if a homeowner defaults on their mortgage. It’s typically required for conventional loans when the down payment is less than 20% of the home’s purchase price, meaning the Loan-to-Value (LTV) is greater than 80%.

- Points: Fees paid to the lender at closing to either lower your interest rate (discount points) or cover loan origination expenses (origination points). One point equals 1% of the loan amount.

- Prepayment Penalty: A specific fee charged by some lenders if you pay off your mortgage loan early, typically within the first few years.

- Principal: The original amount of money borrowed, or the remaining balance of the loan, on which interest is calculated.

- Refinance: The process of replacing an existing home loan with a new one, often with different terms or interest rates.

- Underwriting: The comprehensive process by which a lender assesses the creditworthiness of a borrower and evaluates the risk of lending money to them.

Important Legal and Financial Disclaimer

This mortgage refinance calculator and all the information provided on this page are for illustrative and educational purposes only and do not constitute financial, tax, or legal advice. The results presented are estimates based solely on the inputs you provide and may not reflect all your individual circumstances. Accuracy is not guaranteed. We strongly recommend consulting with a qualified mortgage advisor, tax professional, or financial planner before making any significant financial decisions related to your home loan refinance. All loan products are subject to specific lender terms, credit approval, and property approval. Your financial situation is unique, and personalized, professional advice is essential for making the best choices for your future.

Conclusion: Your Path to Optimized Homeownership

The decision to embark on a mortgage refinance is complex, with far-reaching implications for your financial health. It’s not just about securing a lower rate; it’s about strategically managing your largest debt, unlocking home equity, and aligning your home loan with your evolving life goals.

Whether you’re seeking to reduce your monthly payments, accelerate your path to debt freedom, or access cash for crucial investments, our Advanced Mortgage Refinance Calculator is designed to be your indispensable guide. By providing unparalleled depth in its analysis—from precise breakeven point calculations and intelligent PMI logic to sophisticated tax deduction simulation and transparent cash-out principal breakdowns—this mortgage refinance calculator empowers you with the clarity needed to make truly informed decisions.

We stand firm on our commitment to your privacy, ensuring that your financial data remains yours alone as you explore countless “what-if” scenarios. Use this home loan refinance calculator to demystify the complexities, weigh the pros and cons tailored to your situation, and visualize the long-term impact of your choices. Armed with these insights, you can confidently navigate the refinance journey and optimize your homeownership experience for a more secure financial future.

Start calculating your potential mortgage refinance savings today!