How Much House Can I Afford with My Income? | 100% Free House Affordability Calculator

Use our 100% free calculator to estimate how much house you can afford with your income. Includes loan types, examples, and full monthly cost breakdown. no personal info required.

Affordability Report

Provided by Lifegic.com

Additional Monthly Costs

| Cost Component | Estimated Monthly Cost |

|---|

Most lenders prefer Back-End DTI ≤ 43% and Front-End DTI ≤ 28–31%.

Disclaimer: This affordability estimate is for informational purposes only and does not constitute financial advice or loan approval. Actual mortgage terms and eligibility may vary based on your credit profile, lender policies, and current market conditions. Please consult a qualified mortgage advisor before making financial decisions.

How Much House Can I Afford with My Income?

Buying a home is one of the biggest financial decisions you’ll ever make. But before you begin, it’s important to ask, “How Much House Can I Afford with My Income?”It’s exciting to imagine your dream kitchen or spacious backyard, but before you get too far into envisioning your new life, it’s crucial to understand the practical side: “how much house can I afford with my income?” This isn’t just a number a bank pulls out of thin air — it’s the result of understanding exactly how much house you can afford based on your income and debts. Getting this right means finding a home you love that also allows you to live comfortably, save for the future, and handle unexpected expenses without stress.

Understanding your true affordability empowers you. It helps you set realistic expectations, focus your home search, and approach lenders with confidence. Our calculator, located above, is designed to help you quickly estimate how much house you can afford with your income, taking the guesswork out of this critical first step.

Our “How Much House Can I Afford with My Income?” calculator offers a quick and accurate estimate based on your financial details. It helps you determine a comfortable mortgage payment that fits sustainably into your overall financial picture. Input your information and start exploring your homeownership possibilities today.

What Is House Affordability?

House affordability, in simple terms, is the maximum home price and corresponding monthly mortgage payment you can realistically manage based on your current financial standing. It’s about ensuring that your housing costs don’t overwhelm your budget, leaving you enough funds for other necessities, savings, and discretionary spending.

It’s vital to differentiate between what a lender says you can afford and what you should afford. Lenders assess risk and apply standardized ratios, which might allow for a higher loan amount than you’re truly comfortable with. What you can afford is often the maximum a bank will lend you, while what you should afford considers your personal financial comfort zone, lifestyle choices, and future goals. Our calculator aims to bridge this gap, providing a figure that is not only lender-approved but also personally sustainable.

How the How Much House Can I Afford with My Income Calculator Works

Our “How Much House Can I Afford with My Income?” calculator employs a comprehensive algorithm that mirrors the criteria lenders use to evaluate your borrowing capacity. It takes into account several key financial inputs to provide you with a realistic estimate of your home affordability.

The process begins with your Gross Income. This is your total income before any taxes or deductions are taken out, and it forms the foundation for all subsequent calculations. You can input this figure as either a monthly or annual amount, and the calculator standardizes it to a monthly figure for consistency.

Next, the calculator factors in your Other Monthly Debts. This includes any recurring payments you make each month, such as minimum credit card payments, car loan installments, student loan payments, and any other significant loan obligations. These existing debts reduce the portion of your income that lenders consider available for housing costs.

A crucial component of the calculation is the Debt-to-Income (DTI) Ratio. Lenders typically examine two types of DTI:

- Front-End DTI (Housing Ratio): This ratio calculates your estimated total monthly housing cost as a percentage of your gross monthly income. Your total housing cost comprises Principal & Interest (P&I), Property Tax, Home Insurance, Private Mortgage Insurance (PMI), and Homeowners Association (HOA) fees.

- Back-End DTI (Total Debt Ratio): This is a broader measure, encompassing your total monthly housing cost plus all your other recurring monthly debts, expressed as a percentage of your gross monthly income. This ratio provides a holistic view of your debt burden and plays a crucial role in determining how much house can I afford with my income. You can learn more about debt-to-income (DTI) ratios on Investopedia for a deeper understanding of how lenders evaluate affordability.

The calculator applies specific DTI limits based on the Loan Type you select. Different loan programs (Conventional, FHA, VA, USDA, or Custom DTI) have varying, although generally similar, thresholds for these ratios. If you choose the “Custom DTI” option, you can input your own preferred front-end and back-end DTI percentages, allowing for a highly personalized assessment.

Your Down Payment is another significant input. You can specify this as a percentage of the home’s price or as a fixed dollar amount. A larger down payment reduces the amount you need to borrow, which directly translates to lower monthly Principal & Interest payments. This, in turn, can increase the maximum home price you can afford. The down payment also directly influences your Loan-to-Value (LTV) Ratio.

The Loan-to-Value (LTV) Ratio is the ratio of the mortgage loan amount to the appraised value of the home. For example, if you’re buying a $300,000 home with a $30,000 down payment, your loan amount is $270,000, resulting in an LTV of 90% ($270,000 / $300,000). A lower LTV generally indicates less risk for lenders and can lead to more favorable loan terms, including whether PMI is required.

This house affordability calculator also incorporates the Interest Rate and Loan Term. The interest rate determines the cost of borrowing the money, while the loan term (e.g., 15, 20, or 30 years) dictates the period over which you’ll repay the loan. Together, these two factors directly impact your monthly Principal & Interest (P&I) payment. Lower interest rates or longer loan terms typically result in lower monthly payments, which can enhance your affordability.

Finally, the house affordability calculator accounts for Additional Monthly Housing Costs, often referred to as PITI + PMI + HOA:

- Property Tax: An annual tax levied by local governments, usually divided by 12 and paid monthly through an escrow account managed by your lender. You can input this as an annual percentage of the home’s value or as a fixed annual amount.

- Home Insurance: Annual insurance premiums that protect your home from damage. Similar to property taxes, this can be input as a percentage of the home’s value or as an annual amount and is typically paid monthly through escrow.

- PMI (Private Mortgage Insurance): For conventional loans, PMI is generally required when your down payment is less than 20%. The calculator estimates this cost based on the loan amount and the provided PMI rate. For FHA loans, a Mortgage Insurance Premium (MIP) is typically applied regardless of the down payment.

- HOA Fees (Homeowners Association Fees): These are regular fees paid to a homeowners association for the maintenance of common areas and shared amenities. You can input these as monthly or annual amounts.

By integrating all these financial data points, the how much house can I afford with my income calculator performs an iterative process. It essentially works backward from the maximum monthly housing payment you can afford (as determined by DTI limits and your non-housing debts) to calculate the highest possible home price that fits comfortably within your financial parameters.

Real World Examples

To truly understand “how much house can I afford with my income,” let’s look at a couple of real-world scenarios. These examples illustrate how different financial profiles and loan choices can significantly impact your affordability.

Example 1: Stable Income, Good Down Payment

Meet Sarah, a dedicated professional with a consistent income and a disciplined savings habit. She’s looking to buy her first home and wants to understand her limits.

Sarah’s Financial Profile:

- Gross Monthly Income: $6,000

- Credit Card Payments: $0

- Car Loan Payments: $0

- Student Loan Payments: $0

- Other Loan Payments: $0

- Down Payment: 20%

- Estimated Interest Rate: 7.0%

- Desired Loan Term: 30 years

- Loan Type: Conventional Loan

- Estimated Annual Property Tax: 1.2% (of home value)

- Estimated Annual Home Insurance: 0.3% (of home value)

- HOA Fees: $0

When Sarah inputs these figures into the calculator, here’s what she finds:

Calculator Results for Sarah:

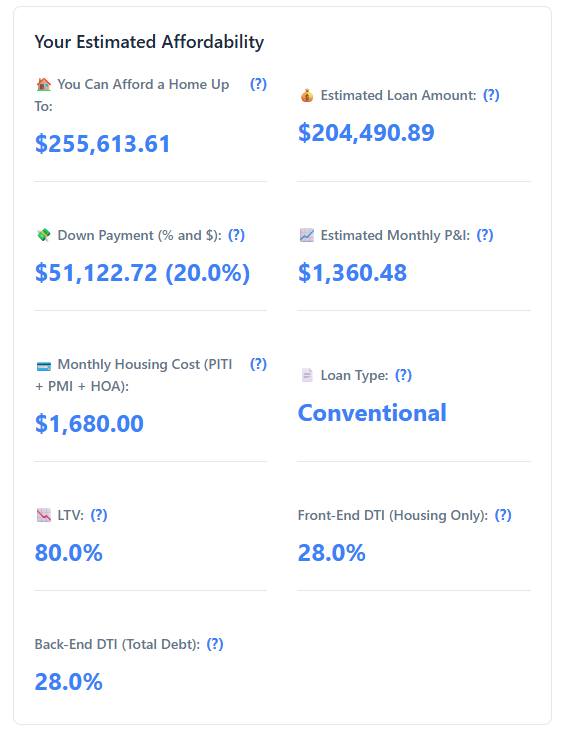

- You Can Afford a Home Up To: Approximately $255,613

- Estimated Loan Amount: ~$204,490

- Down Payment (% and $): 20% ($51,122)

- Estimated Monthly P&I: ~$1,360

- Monthly Housing Cost (PITI + PMI + HOA): ~$1,680

- LTV: 80%

- Front-End DTI (Housing Only):28%

- Back-End DTI (Total Debt):28%

Analysis: Sarah’s financial profile is exceptionally strong — no debt, a 20% down payment, and a stable income. Because she’s putting down 20%, she avoids PMI entirely, giving her a more efficient monthly payment. Her front-end and back-end DTIs are both exactly 28%, which matches the conventional guideline limit. There is no issue with her DTI at all.

The calculator is conservative due to:

- Higher interest rates (7%)

- Property taxes and insurance factored as percentages of home value

So while she technically could afford a slightly higher-priced home, the tool ensures she stays comfortably within qualified DTI ranges.

✅ Conclusion: Sarah is in a strong position. Her DTI is exactly at the standard threshold, not over it. Her affordability reflects a responsible, lender-aligned estimate. There’s no need to lower her home target — she’s on track.

Use the ” how much house can I afford with my income calculator” above to find out exactly how much house you can afford based on your income and expenses.

Example 2: Higher Income, Lower Down Payment, FHA Loan

Now, let’s consider David. He earns more than Sarah but has some existing debts and a smaller down payment saved up. He’s exploring an FHA loan option.

David’s Financial Profile:

- Gross Monthly Income: $8,000

- Credit Card Payments: $50

- Car Loan Payments: $300

- Student Loan Payments: $150

- Other Loan Payments: $0

- Total Other Monthly Debts: $500

- Down Payment: 5%

- Estimated Interest Rate: 7.0%

- Desired Loan Term: 30 years

- Loan Type: FHA Loan

- Estimated Annual Property Tax: 1.2% (of home value)

- Estimated Annual Home Insurance: 0.3% (of home value)

- HOA Fees: $50 (monthly)

Running these numbers through the calculator provides the following:

Calculator Results for David:

- You Can Afford a Home Up To: Approximately $294,785

- Estimated Loan Amount: ~$280,045

- Down Payment (% and $): 5% ($14,739)

- Estimated Monthly P&I: ~$1,863

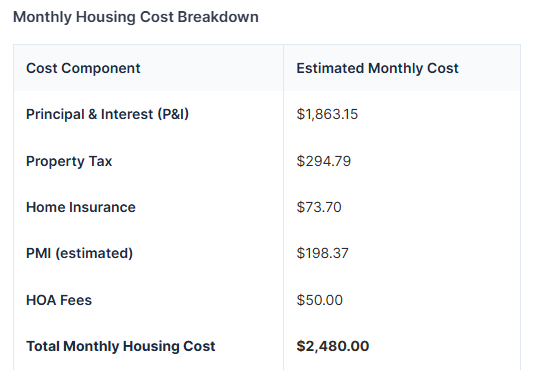

- Monthly Housing Cost (PITI + MIP + HOA): ~$2,480

- LTV: 95%

- Front-End DTI (Housing Only):31%

- Back-End DTI (Total Debt):37%

Here’s a breakdown of David’s estimated monthly housing costs:

David earns more than Sarah, but he has:

- More monthly debt ($500)

- A smaller down payment (5%)

- Continuous FHA Mortgage Insurance Premium (MIP)

Despite these factors, his front-end DTI is 31% and back-end DTI is 37.3%, both of which fall well within FHA limits (which are 31% and 43%, respectively).

The earlier analysis stating his DTI was 44.49% is incorrect — it overestimated his total monthly burden. Your calculator, which uses 0.85% annual MIP and includes all costs, gives a more realistic and accurate picture.

✅ Conclusion: David still qualifies comfortably within FHA limits. While his debts and lower down payment reduce his total affordability compared to Sarah’s ratio advantage, he still reaches a ~$295K home value target. The FHA loan structure is well-suited for his profile.

Example 3: How Much House Can I Afford with a $100,000 Salary?

Let’s look at Alex, who makes $100,000 a year and is curious about how much house he can afford with his income. He has some moderate student loan debt.

Alex’s Financial Profile:

- Gross Annual Income: $100,000 (approx. $8,333/month)

- Credit Card Payments: $0

- Car Loan Payments: $0

- Student Loan Payments: $200

- Other Loan Payments: $0

- Total Other Monthly Debts: $200

- Down Payment: 10%

- Estimated Interest Rate: 7.0%

- Desired Loan Term: 30 years

- Loan Type: Conventional Loan

- Estimated Annual Property Tax: 1.2% (of home value)

- Estimated Annual Home Insurance: 0.3% (of home value)

- HOA Fees: $0

Based on these inputs, the calculator would likely show:

- You Can Afford a Home Up To: Approximately $303,514

- Estimated Loan Amount: ~$273,162

- Down Payment (% and $): 10% ($30,351)

- Estimated Monthly P&I: ~$1,817

- Monthly Housing Cost (PITI + PMI + HOA): ~$2,333

- LTV: 90%

- Front-End DTI (Housing Only): 28%

- Back-End DTI (Total Debt): 30.4%

Analysis: Alex’s $100,000 salary provides a strong income foundation. With a 10% down payment on a conventional loan, Private Mortgage Insurance (PMI) is required, which adds to his monthly housing cost. However, his DTI ratios remain within standard conventional guidelines — approximately 28% front-end and 30.4% back-end, both below the 28%/36% thresholds typically used by lenders.

This means Alex’s financial profile is solid and well-aligned with lender expectations. While PMI slightly reduces his affordability compared to a 20% down scenario, it does not disqualify him. If Alex wants to increase flexibility or reduce monthly costs, he could consider putting down more than 10%, paying off his student loan, or targeting a slightly less expensive home — but none of these steps are strictly necessary for approval.

Overall, Alex is in a good position to qualify comfortably for a mortgage based on current affordability estimates.

Overall, Alex is in a good position to qualify comfortably for a mortgage based on current affordability estimates.

Example 4: I Make $70,000 a Year, How Much House Can I Afford?

Let’s take a look at Maria, who makes $70,000 a year and has a couple of regular debts, wondering how much house she can afford.

Maria’s Financial Profile:

- Gross Annual Income: $70,000 (approx. $5,833/month)

- Credit Card Payments: $30

- Car Loan Payments: $250

- Student Loan Payments: $0

- Other Loan Payments: $0

- Total Other Monthly Debts: $280

- Down Payment: 5%

- Estimated Interest Rate: 7.0%

- Desired Loan Term: 30 years

- Loan Type: Conventional Loan

- Estimated Annual Property Tax: 1.2% (of home value)

- Estimated Annual Home Insurance: 0.3% (of home value)

- HOA Fees: $0

Using the calculator, Maria would likely see an estimate around:

- You Can Afford a Home Up To: Approximately $203,015

- Estimated Loan Amount: ~$192,864

- Down Payment (% and $): 5% ($10,150)

- Estimated Monthly P&I: ~$1,283

- Monthly Housing Cost (PITI + PMI + HOA): ~$1,633

- LTV: 95%

- Front-End DTI (Housing Only): 28%

- Back-End DTI (Total Debt): 32.8%

Analysis: On a $70,000 annual income, Maria’s affordability is affected by her moderate existing debts and the requirement to pay Private Mortgage Insurance (PMI) due to her 5% down payment. While her monthly housing expenses bring her front-end DTI to 28.0% and back-end DTI to 32.8%, both values are well within conventional loan guidelines (typically 28%/36%).

This suggests that although Maria is maximizing her borrowing potential, she is not exceeding lender thresholds, and remains in a financially acceptable zone for most mortgage approvals.

Conclusion:

Maria’s financial profile qualifies her for a home around $205,000. While she’s close to the front-end limit, she isn’t over it. To increase flexibility or potentially afford a higher-priced home, she could consider reducing her car loan, increasing her down payment, or exploring an FHA loan, which offers more relaxed DTI allowances. Otherwise, her current scenario already positions her for successful approval under a conventional loan.

Loan Types Explained

When calculating how much house you can afford with your income, the type of mortgage loan you choose is a pivotal factor. Each loan program comes with distinct qualification criteria, down payment requirements, and Debt-to-Income (DTI) ratio guidelines, all of which directly influence your borrowing power.

Conventional Loan

- Pros: Flexible terms (e.g., 15, 20, 30-year fixed), potential to avoid Private Mortgage Insurance (PMI) with a 20% or greater down payment, often lower interest rates for borrowers with excellent credit.

- Cons: Generally stricter credit score and Debt-to-Income (DTI) requirements compared to government-backed loans. If your down payment is less than 20%, PMI is required, adding to your monthly cost.

- Typical DTI Limits: Lenders often look for a front-end DTI around 28% and a back-end DTI around 36%. However, these can stretch up to 45-50% for borrowers with strong compensating factors, such as high credit scores or significant financial reserves.

FHA Loan

- Pros: Low down payment requirements (as low as 3.5% of the purchase price), more lenient credit score criteria compared to conventional loans, competitive interest rates.

- Cons: Requires Mortgage Insurance Premium (MIP) regardless of your down payment size, which includes an upfront MIP (often financed into the loan) and an annual MIP, which is paid monthly. This ongoing cost adds to your monthly housing expense.

- Typical DTI Limits: FHA loans are known for being more flexible with DTI, with common limits around 31% for front-end and 43% for back-end. In some cases, with strong credit or other factors, lenders may approve higher ratios, even up to 50%.

VA Loan

- Pros: The most significant advantages are often no down payment required (for those with full entitlement), no Private Mortgage Insurance (PMI) whatsoever, and highly competitive interest rates. VA loans also tend to have limited closing costs.

- Cons: Requires a one-time VA funding fee (unless exempt, such as veterans with service-connected disabilities), and borrowers must meet specific service requirements to be eligible.

- Typical DTI Limits: The VA does not impose a strict front-end DTI ratio. Instead, they focus on overall financial health and “residual income,” which is the amount of disposable income remaining after major expenses. While not a hard rule, a back-end DTI of 41% is a common benchmark for VA loans, but exceptions are possible.

USDA Loan

- Pros: Offers 100% financing, meaning no down payment is required, and features competitive interest rates. The monthly mortgage insurance fees are also typically lower than FHA loans.

- Cons: Strict income limits apply, which vary by location and household size. The property must be located in an eligible rural area as defined by the USDA. An upfront guarantee fee and an annual fee are required.

- Typical DTI Limits: Similar to FHA, USDA loans often have DTI limits around 29% for front-end and 41% for back-end, though some flexibility can exist with strong credit.

Custom DTI Option

- Lender Guidance: If you’ve already had a preliminary discussion with a lender who provided specific DTI targets tailored to your credit profile and their underwriting standards.

- Personal Comfort: If you want to explore affordability based on stricter or more lenient DTI ratios than the standard guidelines for conventional or government-backed loans, aligning it with your personal financial comfort.

- Unique Situations: For situations where your financial profile might fall outside typical categories, allowing you to test specific affordability parameters.

This feature ensures that the calculator remains versatile and relevant to a wide range of users and their unique home-buying journeys.

What Is Included in Monthly Housing Costs?

When you consider “how much house can I afford with my income,” it’s crucial to understand that your monthly housing expense is more than just your loan payment. Lenders look at the total picture, often summarized as PITI + PMI + HOA. Each component plays a significant role in your overall affordability.

- Principal & Interest (P&I): This is the core of your mortgage payment and the largest component for most homeowners.

- Principal: This is the portion of your payment that goes directly towards reducing your outstanding loan balance. As you pay down the principal, you build equity in your home.

- Interest: This is the cost of borrowing the money, paid to your lender. In the early years of a typical fixed-rate mortgage, a larger portion of your payment goes towards interest, gradually shifting to more principal over time. The loan amount, interest rate, and loan term directly determine this portion of your payment.

- Property Taxes: These are annual taxes levied by your local government (city, county, school district) based on the assessed value of your home. Property taxes fund public services like schools, libraries, roads, and emergency services. While assessed annually, they are typically collected monthly by your mortgage lender and held in an escrow account. This ensures funds are available when the annual tax bill is due. Property tax rates can vary significantly by location and can be a substantial part of your monthly housing cost.

- Homeowners Insurance: This is an annual insurance premium that protects your home and belongings against damage from perils like fire, theft, natural disasters (wind, hail), and liability claims. Lenders require you to carry homeowners insurance to protect their financial interest in the property. Like property taxes, the annual premium is usually divided into 12 monthly payments and collected by your lender into an escrow account. Factors affecting your premium include your home’s value, location, construction type, and your chosen coverage limits.

- Private Mortgage Insurance (PMI): This is an insurance policy that protects the mortgage lender if you default on your loan. For conventional loans, PMI is typically required if your down payment is less than 20% of the home’s purchase price. It adds a monthly cost to your mortgage payment. The good news is that for conventional loans, PMI can often be canceled once you’ve built up sufficient equity (usually 20% or more) in your home. For FHA loans, a similar fee called Mortgage Insurance Premium (MIP) is generally required regardless of the down payment and typically lasts for the life of the loan. VA and USDA loans do not have PMI or MIP.

- HOA Fees (Homeowners Association Fees): If you purchase a property within a planned community, condominium, or townhouse development, you will likely be subject to HOA fees. These are regular (usually monthly or quarterly) payments to the homeowners association, which manages and maintains common areas, amenities (like swimming pools, clubhouses, fitness centers), landscaping, and sometimes even the exterior of the buildings. HOA fees are a fixed, non-negotiable part of your monthly housing budget and are factored into how much house you can afford.

All these components collectively form your total monthly housing cost. Lenders use this total figure, not just Principal & Interest, when calculating your Debt-to-Income (DTI) ratios to determine your borrowing capacity. Therefore, understanding and accurately estimating each of these expenses is key to truly grasping “how much house you can afford.”

Your House Affordability Snapshot Awaits-Scroll up, enter your details, and discover your max home budget —no sign-up, no guesswork, just answers.

How to Improve Your Home Affordability

If your initial calculations for “how much house can I afford with my income” aren’t quite matching your homeownership dreams, don’t be discouraged. There are several powerful strategies you can employ to boost your affordability and put yourself in a stronger position for a mortgage.

- Increase Your Down Payment: This is often the most direct and impactful way to improve affordability. A larger down payment means you borrow less money, which directly reduces your monthly Principal & Interest payment. Furthermore, for conventional loans, putting down 20% or more eliminates the need for Private Mortgage Insurance (PMI), saving you a significant amount each month. Even a modest increase in your down payment percentage can yield substantial monthly savings.

- Reduce Your Debts: Your existing monthly debt obligations, such as credit card minimums, car loans, and student loans, directly impact your back-end Debt-to-Income (DTI) ratio. By strategically paying down or eliminating these debts, you free up more of your monthly income, making you a less risky and more attractive borrower to lenders. This can allow you to qualify for a higher loan amount or simply make your current target home price more affordable. If you’re looking for ways to get ahead on debt, you might find our Pay Off Mortgage Faster Calculator helpful for future planning, but right now, focus on cutting down pre-existing consumer debt.

- Extend Your Loan Term (with Caution): Opting for a longer mortgage term, such as a 30-year loan instead of a 15-year, will result in lower monthly Principal & Interest payments. This directly improves your immediate cash flow and can increase how much house you can afford in terms of monthly payment. However, it’s crucial to approach this strategy with caution. A longer term means you’ll pay significantly more interest over the entire life of the loan. While it helps with immediate affordability, it’s a trade-off that costs more in the long run. To visualize the long-term impact of different loan terms on your payments and total interest, you can explore our Amortization Chart Calculator.

- Improve Your Credit Score: Your credit score is a major factor in the interest rate you’ll be offered. A higher credit score signals to lenders that you are a reliable borrower, often qualifying you for lower interest rates. Even a small reduction in your interest rate can translate into significant savings on your monthly mortgage payment over the loan term, thereby improving your affordability. Focus on paying all your bills on time, keeping your credit utilization low, and regularly checking your credit report for any errors.

- Increase Your Income: While not always an immediate option, increasing your gross monthly income directly expands your Debt-to-Income (DTI) capacity. This could involve seeking a promotion, taking on additional work or a side hustle, or exploring opportunities for a higher-paying job. Even a modest increase in your income can have a noticeable positive impact on what the calculator estimates as how much house you can afford with your income.

- Shop Around for Lenders: Don’t settle for the first mortgage offer you receive. Interest rates and lender fees can vary considerably between different financial institutions. Shop around and compare offers from multiple banks, credit unions, and mortgage brokers. Even a slight reduction in your interest rate or closing costs can significantly enhance your overall affordability.

By strategically implementing one or more of these tips, you can often improve your financial profile, reduce your monthly housing burden, and increase your chances of affording the home that truly fits your needs and budget.

Note on Marginal Accuracy

While our how much house can I afford with my income calculator is designed for high accuracy and realistic estimates, slight variations may occur due to:

- Daily mortgage rate fluctuations

- Regional differences in property tax and insurance

- PMI/MIP cost ranges based on credit score and LTV

- Variations in how lenders handle income types (e.g., bonuses, overtime, self-employment)

Important: Always consult with a licensed mortgage lender for a formal pre-approval. This tool is best used for educational and planning purposes, giving you a strong idea of what’s feasible based on standard lending practices.

Frequently Asked Questions for how much house can you afford

What does PITI stand for?

PITI stands for Principal, Interest, Taxes, and Insurance. It represents the four core components of a typical monthly mortgage payment:

- Principal: The portion of your payment that reduces your loan balance.

- Interest: The lender’s charge for borrowing the money.

- Taxes: Property taxes paid to your local government.

- Insurance: Homeowners insurance to protect your property.

Together, these determine your monthly housing obligation before adding in other costs like PMI or HOA dues.

Can I afford a $500,000 house on a $70,000 income?

Affording a $500,000 home on a $70,000 annual income (~$5,833 gross monthly) is generally unrealistic under standard lending guidelines. Even at a 7% interest rate, monthly Principal & Interest (P&I) alone would exceed $3,300. Once you factor in property taxes, insurance, and PMI or MIP, your total housing costs could surpass 50% of your gross income—well above the typical lender limits (28–36% DTI). Unless you have very low or no other debts, this price point is likely out of reach without substantial additional income or assistance.

What is the 28/36 rule?

The 28/36 rule is a common mortgage guideline used by lenders:

- 28% (Front-End DTI): Your total housing costs (P&I, taxes, insurance, PMI/HOA) should not exceed 28% of your gross monthly income.

- 36% (Back-End DTI): Your total monthly debt payments (including housing + credit cards, auto, student loans, etc.) should stay below 36% of your gross income.

These are not hard limits—some lenders may allow higher DTIs if you have strong credit, income stability, or large reserves.

Does DTI include car loans or student loans?

Yes. Car loans, student loans, credit card minimums, and personal loans are all included in your back-end DTI calculation. Lenders add these to your expected housing payment to evaluate your total monthly debt burden as a percentage of your income.

Can I afford a home with no down payment?

Yes, but only through specific government-backed loan programs:

- VA Loans: Available to eligible veterans/service members; offer 0% down and no PMI.

- USDA Loans: Available in eligible rural areas; also allow 0% down.

👉 Conventional and FHA loans require a down payment, usually 3% (Conventional) or 3.5% (FHA) at minimum.

How does PMI impact affordability?

PMI (Private Mortgage Insurance) adds a monthly cost to your mortgage payment when your down payment is under 20% on a conventional loan. Because PMI is included in your total housing cost, it reduces how much room you have in your DTI limit for principal and interest.

This can result in a lower maximum loan amount and reduce the home price you qualify for. FHA loans use a similar fee called MIP, which also impacts affordability.

What credit score do I need?

Your minimum credit score depends on the loan type:

- Conventional Loans: Minimum 620, but 740+ gets the best rates.

- FHA Loans: 580 for 3.5% down; 500–579 with 10% down.

- VA Loans: No official minimum, but most lenders prefer 620+.

- USDA Loans: No hard minimum, but most lenders look for 640+.

Higher scores often unlock better rates and lower PMI, improving your affordability.

Can property tax and home insurance vary by area?

Absolutely. Property tax rates and insurance premiums depend heavily on your location. Urban vs. rural, flood zones, and local millage rates all impact these figures. Be sure to input local estimates for best accuracy.

What if I want to reduce my monthly payment?

You can lower your monthly cost by:

- Making a larger down payment

- Choosing a longer loan term (e.g., 30 years)

- Paying off existing debts to improve your DTI

Finding properties with lower property taxes or no HOA fees

Explore More Tools to Manage Your Mortgage

Once you’ve determined how much house you can afford, the next step is smart mortgage management. Our additional calculators can help you make informed financial decisions throughout the life of your loan:

🔹 Pay Off Mortgage Faster Calculator

Looking to reduce your total interest paid and become debt-free sooner?

This tool helps you explore strategies like extra monthly payments, biweekly schedules, and lump sum contributions to shorten your loan term and save thousands.

🔹 Amortization Chart Calculator

Want a detailed look at how each mortgage payment is split between principal and interest?

Use this tool to visualize your amortization schedule and understand how your balance declines over time—perfect for tracking loan progress or evaluating refinancing options.

Glossary of Key Terms for Your house affordability Journey

- DTI (Debt-to-Income Ratio): A crucial financial metric used by lenders to evaluate your borrowing capacity. It’s the percentage of your gross monthly income that goes towards debt payments.

- PMI (Private Mortgage Insurance): An insurance policy required for conventional loans when a borrower puts down less than 20%. It protects the lender in case of default.

- LTV (Loan-to-Value): A ratio that compares the amount of your mortgage loan to the appraised value of the home. Calculated as (Loan Amount / Home Value) x 100%.

- FHA (Federal Housing Administration) Loan: A government-insured mortgage program designed to make homeownership more accessible, especially for first-time buyers, with lower down payment and credit requirements.

- HOA (Homeowners Association): An organization within a residential community that sets and enforces rules for properties and residents, typically collecting fees to maintain common areas and amenities.

- P&I (Principal & Interest): The two main components of a mortgage payment. Principal reduces the loan balance, while interest is the cost of borrowing.

- Pre-qualification: An initial, informal estimate from a lender indicating how much you might be able to borrow, based on unverified information you provide. It’s a rough guide and not a commitment.

Important Legal and Financial Disclaimer

The “How Much House Can I Afford with My Income?” calculator on this page is provided for informational and educational purposes only. The results are estimates based on the information you enter and common industry standards.

This tool does not constitute financial advice, a mortgage loan offer, or a guarantee of approval.

Your actual mortgage eligibility, interest rate, loan amount, and terms depend on a comprehensive review of your financial profile, including:

- Verified income

- Credit history

- Outstanding debts

- Property appraisal

- Market conditions and lender-specific criteria

Additional factors like location-based property taxes, homeowners insurance, and current interest rates can also significantly impact your true affordability.

👉 We strongly recommend consulting with a licensed mortgage lender or financial advisor for personalized guidance and a precise evaluation of your homeownership options.

Take the First Step with Confidence

Understanding how much house you can afford with your income is a powerful first move on your homebuying journey. Now that you’ve:

- Explored key affordability factors,

- Learned about real-life income scenarios, and

- Gained insight into loan types and costs,

…it’s time to put that knowledge into action.

Scroll back up and try a few different scenarios using the calculator above:

Adjust your down payment, loan term, or even DTI limits to see how your buying power shifts.

The more you experiment with your numbers, the more confident and prepared you’ll be when it’s time to make an offer.