Interest on Interest Calculator – Free Online Compounding Growth Calculator

Use our free online Interest-on-Interest Calculator to see how compounding grows your savings faster. Calculate with flexible contributions, multiple compounding options, and instant results.

Interest on Interest Calculator – Compound Growth Tool

Understanding how your money grows over time is a cornerstone of financial literacy, and few concepts are more powerful than “interest on interest.” It’s the secret engine that turns modest, consistent savings into substantial long-term wealth. Our comprehensive interest on interest calculator is designed to demystify this process, giving you a clear, visual breakdown of your potential investment growth.

This tool goes beyond a simple interest calculator compounding for a lump sum. It empowers you to see the true impact of factors like regular contributions, varying compounding frequencies, and even the drag of inflation and taxes. By using this powerful investment growth calculator, you can plan for retirement, a down payment on a home, or any other significant financial goal with greater clarity and confidence. The best way to use this calculator is to test a few scenarios to find a plan that works best for your financial situation.

What is an Interest-on-Interest Calculator?

An interest on interest calculator is a specialized financial tool that models the exponential growth of an investment over time. While a basic interest calculator might show you the returns on your initial deposit, this advanced tool specifically tracks and quantifies the compounding effect. It clearly separates your final investment value into three key components: your original principal, the sum of your contributions, and the total interest earned.

The term “interest on interest” refers to the process where the interest you earn is added back to your principal balance. This larger new balance then earns interest in the next period, and so on. This continuous cycle accelerates the growth of your money far beyond what you could achieve with simple interest alone. As such, this tool is vital for anyone engaging in long-term financial planning. It helps you visualize the impact of consistent saving and the sheer power of time.

How Does Interest on Interest Work?

To truly grasp the magic of compounding, let’s look at a simple example without any new contributions. Imagine you invest $1,000 in an account with an annual interest rate of 5% for 3 years. We’ll compare this to a simple interest scenario to highlight the difference.

Year 1: The Foundation

- Simple Interest: You earn 5% on the original $1,000, which is $50. Your new balance is $1,050.

- Compound Interest: You earn 5% on the original $1,000, which is $50. The interest is added to your account, making your new balance $1,050. At this point, there’s no difference.

Year 2: The Start of Compounding

- Simple Interest: You still only earn 5% on the original $1,000, which is another $50. Your balance grows to $1,100.

- Compound Interest: You earn 5% on your new, larger balance of $1,050. This earns you $52.50 in interest ($2.50 of which is “interest on interest”). Your balance is now $1,102.50.

Year 3: The Gap Widens

- Simple Interest: You earn a final $50. Your ending balance is $1,150.

- Compound Interest: You earn 5% on your new balance of $1,102.50. This generates $55.13 in interest. Your final balance is $1,157.63.

Over just three years, the power of compounding earned you an extra $7.63, a difference that becomes exponentially more significant over longer timeframes and with larger amounts. This is the fundamental principle our interest on interest calculator models.

Interest on Interest Formula

The standard compound interest formula is the mathematical foundation for this type of calculation. It determines the future value of an investment based on its present value, rate, and duration. It is expressed as follows:

FV=PV∗(1+i/n)(n∗t)

Let’s break down each component of this powerful formula:

- FV (Future Value): This is the final amount of your investment after the specified period, including both the principal and all accumulated interest. This is the number you’re aiming to find.

- PV (Present Value): This is your initial lump-sum investment or the principal you start with.

- i (Interest Rate): The annual interest rate of your investment, expressed as a decimal (e.g., 7% is 0.07).

- n (Compounding Frequency): This represents the number of times per year the interest is compounded. For example, for a monthly interest calculator compounding, n would be 12. For quarterly, n is 4.

- t (Time): The total number of years your money is invested or borrowed.

This formula works for a single initial investment. Our interest on interest calculator performs a more complex, month-by-month calculation to account for ongoing contributions and other variables, providing a highly accurate projection.

Simple Interest vs. Interest on Interest

The difference between simple interest and compound interest is fundamental to wealth-building. A simple interest calculator compounding on the initial principal is useful for short-term loans or simple savings accounts, but it won’t show you the true long-term potential of your money. The table below provides a clear, side-by-side comparison.

Feature | Simple Interest | Compound Interest (Interest on Interest) |

Calculation Basis | Only on the original principal amount. | On the original principal and all accumulated interest. |

Growth Pattern | Linear; the same amount of interest is earned each period. | Exponential; the interest earned accelerates over time. |

Best for… | Short-term loans, simple transactions. | Long-term investments, retirement savings, mortgages. |

Example | A $10,000 investment at 5% earns exactly $500 per year. | A $10,000 investment at 5% earns more each year as the balance grows. |

The key takeaway is that with simple interest, your money doesn’t have a chance to work for you. With compound interest, your earnings start generating their own earnings. That’s the core of the “interest on interest” concept. This is a critical distinction to grasp before you use any investment calculator online.

How to Use Our Interest on Interest Calculator

Our tool is designed to be intuitive and powerful, allowing you to calculate compound interest with remarkable precision. Here’s a breakdown of each input field and how it influences your results. You can experiment with different numbers to find a solution that works for you.

Core Inputs

- Initial Investment: This is the starting lump sum you’re putting into the investment. It could be an inheritance, a bonus, or the money you already have in an account. Our tool, which doubles as an investment growth calculator, allows you to enter this with or without a dollar sign.

- Annual Interest Rate (%): The percentage rate your investment is expected to earn per year. Be realistic with this number; a long-term average for a diversified stock portfolio might be 7-10%, while a high-yield savings account is typically 3-5%. This is the single most powerful factor for determining how much interest on interest you’ll earn.

- Investment Duration: This is the length of time your money will be invested. Our calculator breaks this down into years and months, giving you total flexibility. The longer your duration, the more pronounced the effect of the compounding frequency.

- Compounding Frequency: This is a crucial setting that determines how often your earned interest is added back to your balance. The more frequently your interest is compounded, the faster your investment grows. Options include:

- Annually (1x/year)

- Semi-Annually (2x/year)

- Quarterly (4x/year)

- Monthly (12x/year)

- Daily (365x/year)

- Daily (Leap Year Adjusted) (365.25x/year)

- Contribution Amount & Frequency: This feature allows you to model regular savings. You can input a recurring amount and choose whether you contribute monthly, quarterly, or annually. This is especially useful for a long-term investment calculator online.

- Contribution Timing: You can specify whether your contributions are made at the Beginning of Period or the End of Period. As you’ll see in your results, contributing at the beginning gives your money more time to compound, leading to slightly higher returns.

Advanced Settings

Clicking the “Advanced Settings” accordion reveals additional options for a more sophisticated financial model.

- Annual Contribution Growth (%): If you expect to increase your savings over time, you can input a percentage here. This is a powerful feature for modeling salary raises and how they can accelerate your growth.

- Annual Tax on Earnings (%): For taxable accounts, you can input an estimated tax rate. The calculator will then deduct a portion of your interest earnings each year, giving you a more realistic “after-tax” projection.

- Annual Inflation Rate (%): This allows you to see the real purchasing power of your money in the future. The calculator will provide an “inflation-adjusted final value” to show you what your investment is worth in today’s dollars. This is a key feature that a basic interest calculator compounding tool often lacks.

Reading the Results Section

After you calculate compound interest, our tool provides a detailed breakdown of your projected growth.

- Final Value: The total projected value of your investment, including all principal and interest.

- Total Principal: The sum of your initial investment and all your contributions. This is the total amount of your own money you put in.

- Total Contributions: The sum of all your periodic contributions.

- Total Interest Earned: The total amount of money generated purely from interest.

- Simple Interest (Non-Compounded): The amount of interest you would have earned if there were no compounding effect, calculated only on your principal and contributions.

- Interest on Interest: This is the most important number in the whole calculation! It’s the difference between your total interest earned and your simple interest. This figure represents the money you earned purely from the power of compounding.

- Inflation-Adjusted Value: This shows you the buying power of your final investment value in today’s dollars, after accounting for the inflation rate.

- Rule of 72 Estimate: A quick-and-dirty estimate of how many years it would take for your initial investment to double.

Example Scenarios: Seeing Interest on Interest Calculator in Action

Using the interest on interest calculator with real numbers can make the concept of compound growth tangible. Let’s walk through a few scenarios to demonstrate the calculator’s power and versatility.

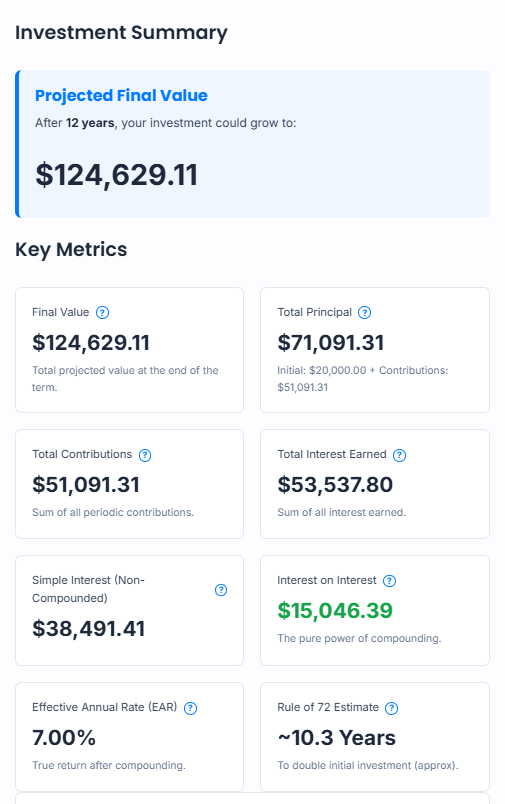

Example 1: Long-Term Retirement Savings

- Initial Investment: $20,000

- Annual Interest Rate: 7%

- Investment Duration: 12 years

- Compounding Frequency: Annually

- Contribution Amount: $300 (monthly)

- Contribution Timing: Beginning of Period

- Annual Contribution Growth: 3%

Outputs:

- Final Value: $124,629.11

- Total Principal: $71,091.31

- Total Interest Earned: $53,537.80

- Interest on Interest: $15,046.39

This example shows how a moderate initial investment, paired with consistent contributions and a solid interest rate, can grow significantly over time. The compounding effect accounts for $15,046.39 of the total interest earned, highlighting the powerful impact of reinvesting earnings

Don’t leave your money’s potential untapped. Try our Interest-on-Interest Calculator today and plan smarter for tomorrow.

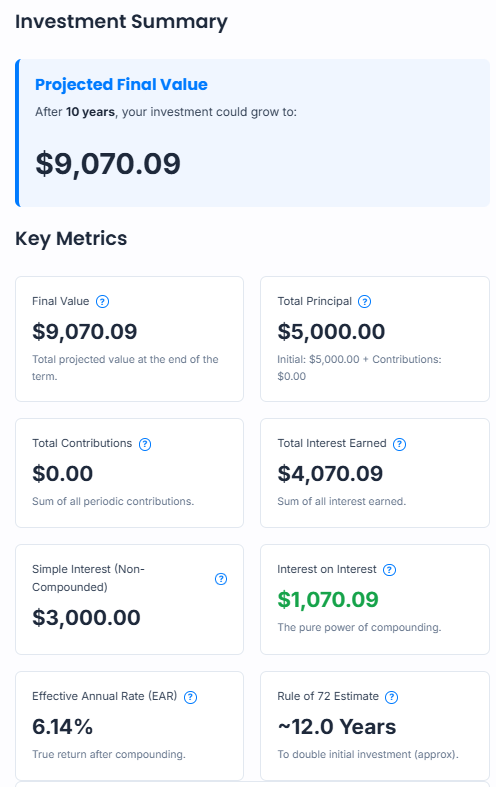

Example 2: Lump-Sum Investment

- Initial Investment: $5,000

- Annual Interest Rate: 6%

- Investment Duration: 10 years

- Compounding Frequency: Quarterly

- Contribution Amount: $0

- Contribution Timing: Not applicable

- Annual Contribution Growth: 0%

Outputs:

- Final Value: $9,070.09

- Total Principal: $5,000.00

- Total Interest Earned: $4,070.09

- Simple Interest: $3,000.00

- Interest on Interest: $1070.09

This example contains no periodic contributions, so all growth comes from the initial lump sum and reinvested interest. The Interest on Interest ($1,070.09) is the extra gain from compounding (i.e., interest earned on previously earned interest). The scenario nicely illustrates how compounding alone (quarterly here) increases returns beyond simple interest over time.

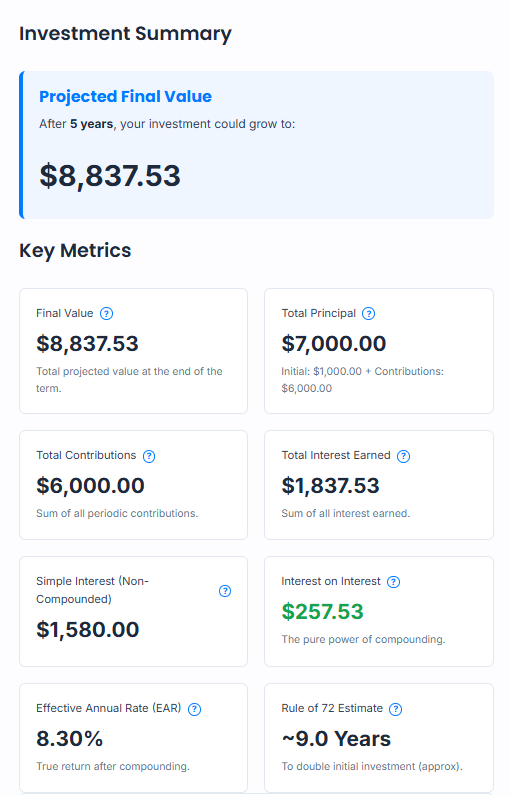

Example 3: Short Term Aggressive Savings

- Initial Investment: $1,000

- Annual Interest Rate: 8%

- Investment Duration: 5 years

- Compounding Frequency: Monthly

- Contribution Amount: $100 (monthly)

- Contribution Timing: End of Period

- Annual Contribution Growth: 0%

Outputs:

- Final Value: $8,837.53

- Total Principal: $7,000.00

- Total Interest Earned: $1,837.53

- Simple Interest: $1580.00

- Interest on Interest: $257.53

Even over a relatively short period, monthly contributions and a high compounding frequency can make a significant difference. In this case, the interest on interest calculator shows that over $257 of the total interest came from the power of compounding alone, proving that every little bit helps, even over shorter timelines.

Benefits of Using an Interest on Interest Calculator

There are many reasons why a tool like this is essential for anyone serious about their finances.

Visualize Compound Growth

A key benefit of this investment calculator online is its ability to visually represent growth over time. The charts in the results section, which show the breakdown between principal and interest, give you a tangible sense of how your money is multiplying. This can be a powerful motivator to stay on track with your savings goals. As your investment duration increases, the interest earned curve starts to steepen, dramatically overtaking the principal contributions line.

Breakdown of Principal, Interest, and Interest-on-Interest

Our calculator’s detailed results table goes far beyond what a basic interest calculator compounding tool can do. By breaking down the final value into its constituent parts—initial investment, contributions, simple interest, and interest on interest—you gain a deeper understanding of where your money is coming from. Seeing a tangible number for “interest on interest” is an empowering experience that highlights the true value of long-term investing.

Investment Planning & Debt Payoff Acceleration

This tool isn’t just for investors. It can also be used as a powerful way to model debt. By treating the loan balance as the initial investment and the interest rate as your debt rate, you can model how making extra contributions (payments) can drastically reduce the total interest paid and accelerate your debt-free date. Whether you’re planning for a goal or tackling debt, this interest on interest calculator is a versatile and essential tool.

Factors That Influence Interest on Interest Growth

To effectively calculate compound interest and project your future wealth, you must understand the key variables that drive the outcome. Each factor plays a crucial role in the speed and scale of your investment’s growth.

Interest Rate

This is arguably the most impactful factor. A higher annual interest rate means your principal and all accumulated interest grow faster, leading to a much larger final balance. For example, a 10% rate will cause your money to grow much faster than a 5% rate, with the difference becoming massive over decades. This is why a simple interest calculator compounding only a single input is insufficient for real-world planning. The interest rate is a multiplier of everything else.

Compounding Frequency

The more frequently your interest is compounded, the sooner your money starts earning interest on itself. This is why daily compounding, for example, will always yield a slightly higher return than annual compounding for the same interest rate. While the difference may seem small in the short term, it can add up to a significant amount over a long-term investment horizon. Our interest on interest calculator handles all major frequencies with precision.

Contribution Amount & Timing

Your regular contributions are the fuel that powers your compounding engine. The more you put in, the larger the base from which interest can be earned. And as our calculator shows, the timing of these contributions matters. Even a slight advantage of contributing at the beginning of the month gives your money an extra period to compound, making a noticeable difference over many years. This is a detail that many basic investment growth calculator tools often overlook.

Investment Duration

Time is the secret ingredient in the compound interest formula. The longer your investment has to grow, the more pronounced the “hockey stick” effect of compounding becomes. Early on, contributions are the primary driver of your account balance. But over decades, the interest on interest portion begins to grow exponentially, eventually becoming the largest component of your final value. This is why starting to save early, even with small amounts, is so critical.

Common Mistakes to Avoid When Calculating Compound Interest

Even with a powerful tool like our interest on interest calculator, it’s easy to make mistakes that can skew your projections. Being aware of these common pitfalls can help you get a more accurate and realistic view of your financial future.

Confusing Annual vs. Monthly Rates

A common error is to input a monthly interest rate into a field that asks for an annual rate. For example, if you have a savings account that pays 0.5% per month, you might be tempted to enter “0.5.” However, the annual interest rate would be 6% (0.5% x 12). Always ensure you’re using the correct annual percentage to get a correct calculation. Our interest calculator compounding tool assumes you are entering the annual rate, which is the industry standard.

Ignoring Contribution Timing Effects

As mentioned earlier, the timing of your contributions—beginning versus end of the period—has a measurable impact on your final balance. Forgetting to account for this can lead to slightly inaccurate projections, especially over many years. It’s a small detail, but it speaks to the power of time and is a nuance our advanced investment growth calculator is built to handle.

Forgetting Tax or Inflation Adjustments

Many people look at a gross final value and forget to consider how inflation and taxes will erode their purchasing power. A $1 million retirement portfolio in 30 years won’t have the same buying power as $1 million today. Similarly, a significant portion of your interest earnings may be owed to the government. Our interest on interest calculator includes these advanced settings so you can model a more realistic, “net” final value. This is crucial for accurate financial planning.

Turn small deposits into big results with the power of compounding- Try it now.

FAQs

What is interest on interest?

Interest on interest is the portion of your total investment earnings that comes from the interest your investment has already generated. It’s the engine of compound growth, where your initial principal earns interest, and that new, larger balance earns even more interest in the next period, creating a virtuous cycle of accelerated growth.

Is this the same as compounding?

Yes. The term “interest on interest” is another way of describing the process of compounding. It highlights the core mechanism where interest is added to the principal and begins to generate its own earnings. Our tool is essentially a sophisticated interest calculator compounding multiple variables at once

How do I manually calculate interest on interest?

While it’s highly tedious, you can calculate the interest on interest manually. You’d need to first calculate compound interest to get your final value and the simple interest on your principal and contributions. Then, subtract the total simple interest from the total compound interest to find the “interest on interest” portion. Our calculator does this instantly for you!

Which compounding frequency gives the highest returns?

For a given interest rate, the more frequently the interest is compounded, the higher your returns will be. Daily compounding will yield more than monthly compounding, which in turn will yield more than annual compounding. The difference may be small in a single year, but it becomes significant over the long term.

Can this be used for loans?

Yes. The same principles apply to loans, but in reverse. For example, if you make extra payments on a loan, you are essentially reducing the principal balance, which in turn reduces the amount of “interest on interest” you will pay over the life of the loan. This can save you a substantial amount of money.

Why are my results different from other calculators?

Our calculator uses a precise, month-by-month calculation engine that accounts for a wide array of variables, including daily compounding, contribution timing, and annual contribution growth. Other simpler calculators may use a single compound interest formula without these nuances, which can lead to slightly different results. Our goal is to provide the most accurate and flexible investment calculator online possible.

Does interest on interest really make a big difference?

Over short periods, the difference may seem small. But over many years, interest on interest can account for a large percentage of your total returns — often more than the original principal. This is why compounding is called the “eighth wonder of the world” in investing circles.

Is interest on interest taxable?

In most countries, yes — any earned interest, including the portion from interest on interest, is subject to income tax unless it’s held in a tax-advantaged account like a retirement fund or specific savings plan.

Does interest on interest apply if I withdraw earnings?

No. If you withdraw your interest regularly, you break the compounding cycle. Only the remaining balance will continue to earn interest, which reduces the interest-on-interest effect significantly

How can I maximize interest on interest?

Increase your compounding frequency, avoid withdrawing earnings, reinvest dividends, and add regular contributions. Time is the most important factor — the longer your money compounds, the greater the effect.

Does inflation affect interest on interest?

Yes. While compounding grows your nominal balance, inflation reduces your purchasing power. The real benefit comes when your compounding rate outpaces inflation over the long term.

Explore More Financial Tools

Our suite of financial tools is designed to help you make smarter financial decisions. After you’ve had a chance to experiment with our interest on interest calculator, check out these other helpful resources.

Important Legal and Financial Disclaimer

The Interest on Interest Calculator is provided for educational and informational purposes only and does not constitute financial, investment, tax, or legal advice. While we strive for accuracy, the results generated are estimates based on the data you provide and certain assumptions about interest rates, compounding frequency, contribution timing, taxes, and inflation. Actual results may vary significantly due to market fluctuations, changes in interest rates, fees, taxes, and other unforeseen factors.

We recommend that you consult a qualified financial advisor or tax professional before making any financial decisions based on these calculations. Past performance of investments does not guarantee future returns, and all investing carries risk, including the potential loss of principal. By using this calculator, you acknowledge that you are solely responsible for any decisions made and that we are not liable for any loss or damages resulting from the use of or reliance on the information provided.

Final Thoughts

The ability to calculate compound interest and visualize the power of “interest on interest” is a critical skill for building long-term wealth. Our calculator is more than just a tool; it’s a financial education resource that empowers you to take control of your financial future.

Whether you’re planning for retirement, saving for a major purchase, or just curious about the potential of your money, this interest on interest calculator gives you the data you need to make informed decisions. We encourage you to test different scenarios and see for yourself how time, interest rates, and consistent saving can work together to turn your financial dreams into a reality.

Learn more about the power of compound interest in this video. The Power of Compound Interest – Investopedia